Editor's Note (June 21, 2026): This is an educational explainer of a recurring market puzzle, anchored to the mid-2026 backdrop. It explains why stocks can rise while rates are high — it does not predict where stocks, rates, or yields go next, and nothing here is investing advice.

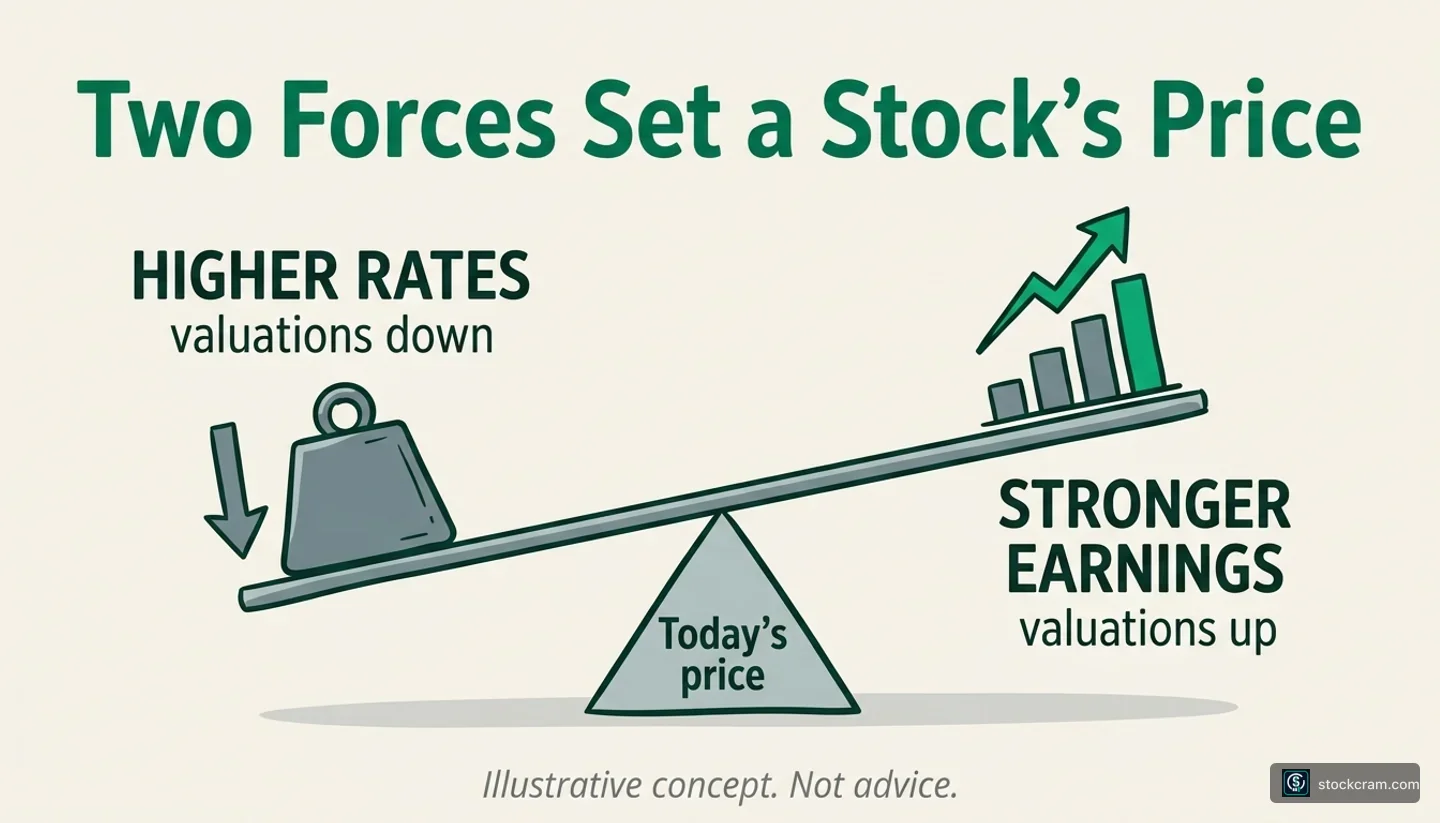

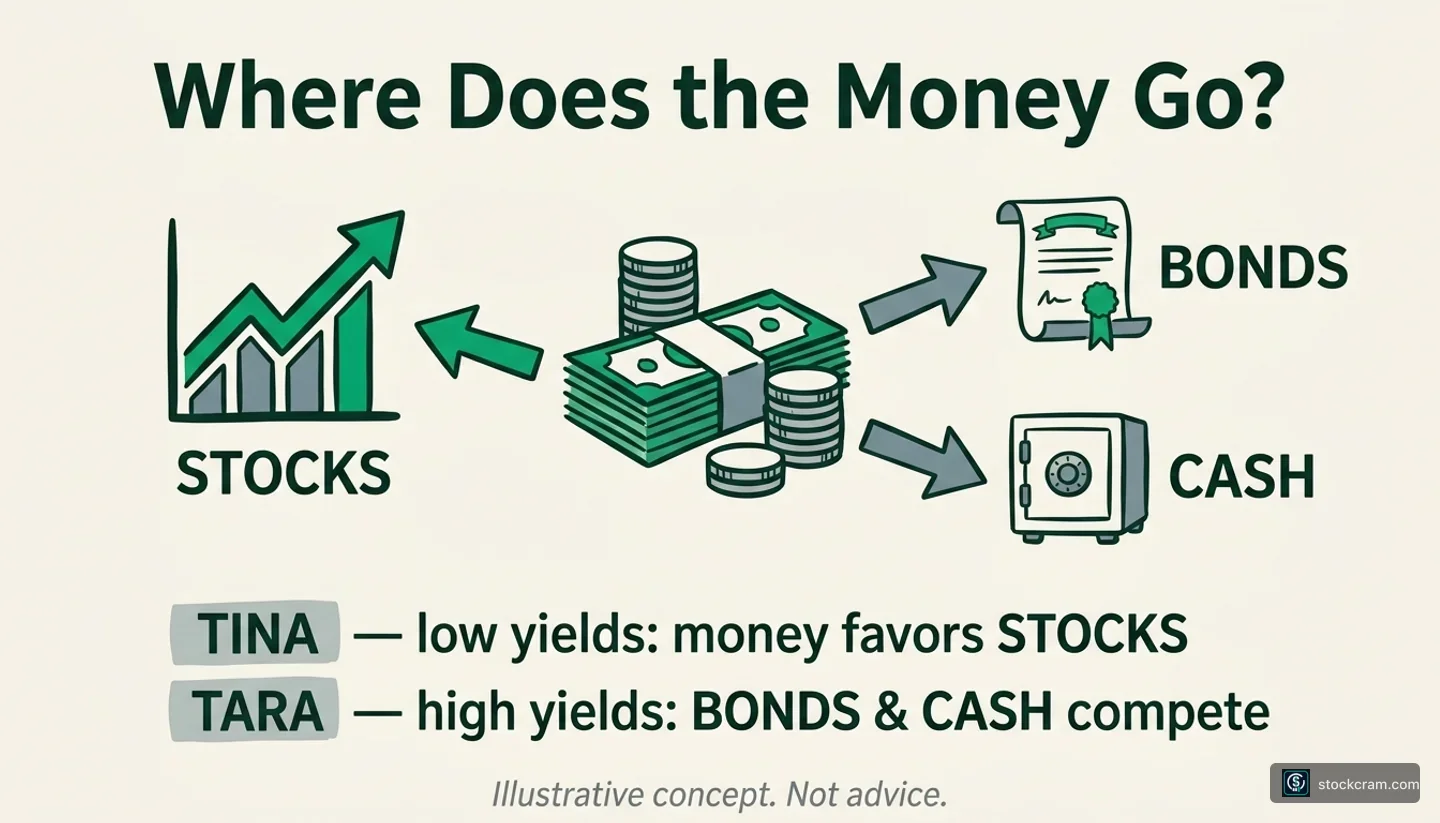

Quick answer: Stocks can go up when interest rates are high because rates are only one of several inputs into stock prices. Higher rates usually lower valuations, but if investors expect company earnings to grow faster, prices can rise anyway. Stocks can also hold up when investors still prefer equities to bonds or cash despite higher yields.

"Higher interest rates are bad for stocks" is one of the first rules of thumb a new investor learns, and it's genuinely useful — there's a real mechanism behind it (the discount-rate rule, below). But it's a tendency, not a law of physics. Rates affect the multiple investors will pay; earnings expectations affect the profits being valued; and sentiment affects both. A stock price is the result of all of them at once.

The mid-2026 backdrop (data as of mid-June 2026): the Federal Reserve held its benchmark at 3.50%–3.75% (FOMC, June 17, 2026); the 10-year Treasury yield sat near 4.5% (FRED series DGS10, mid-June 2026); annual inflation ran at 4.2% (all-items CPI-U, year over year, May 2026, BLS); and the major U.S. indexes were near record highs, up roughly 10% year-to-date (S&P 500 price index — price return, not total return — through June 19, 2026; S&P Dow Jones Indices). High rates, high yields, high stocks — all at once. Here's how that combination is possible, with the bear case included.