Robinhood Agentic Trading: How It Works and the Risks

Robinhood agentic trading lets an AI agent place trades in a dedicated, funded account. A calm, plain-English walkthrough of how it works and the risks.

15 min read

Read Article

SpaceX priced its IPO at $135/share for a record $75B raise, first trade June 12. Here's the lockup schedule, retail-fill math, Day-1 mechanics, and both sides of the valuation debate.

Educational purposes only. This content does not constitute investment advice. Read our disclaimer

StockCram is not a broker-dealer, investment adviser, or financial institution. All content is for educational and informational purposes only and should not be construed as personalized investment advice. Consult a qualified financial professional before making investment decisions. Past performance does not guarantee future results.

On the evening of June 11, 2026, SpaceX officially priced its initial public offering at $135 per share on roughly 556 million shares, raising $75 billion, the largest IPO on record by a wide margin. SPCX began trading June 12 on NASDAQ and closed its first day at $160.95, up about 19%: see the Day-One update below for the full picture. (NPR; CNBC, June 11.)

The 60-second version of the SpaceX IPO debate: Bulls (Wedbush, PIMCO, BlackRock) point to real revenue across launch, Starlink, and AI compute, plus a staggered lockup designed to spread post-IPO selling pressure. Bears (Morningstar most pointedly) call $1.75T valuations overvalued by roughly half. Both sides have real data. Here's the long version, with the lockup schedule, retail-fill math, and Day-1 mechanics most coverage is skipping.

We'll walk through what got priced this evening, what trades tomorrow, what the unusual staggered lockup actually says, how retail allocation math really works, what Day-1 trading mechanics look like (including the LULD halts almost no beginner-facing coverage explains), where SpaceX stands in NASDAQ-100 and S&P 500 inclusion, and what each side is actually arguing. This is Article 2 of our Trillion-Dollar IPO Wave sub-series; for the broader wave context covering Anthropic and OpenAI too, see our wave overview. For the underlying AI bubble debate this wave sits inside, see our bubble piece. One note before we start: first-day trading is now complete; the dated Day-One update just below carries the confirmed result. The pricing, lockup, and index-inclusion analysis throughout reflects reporting as of June 11–12, 2026; we mark inference clearly throughout, and the explicitly dated snapshot sections ("as of June 11") are kept as an honest record of what was known at pricing.

Before the long version, the wave at a glance: read this and skip ahead if you're short on time, or keep going for the lockup schedule, retail-fill math, and Day-1 trading mechanics.

The headline numbers, all confirmed at pricing tonight. SpaceX is selling 555.6 million shares at a fixed $135 each, raising $75 billion at a $1.75 trillion target valuation. Underwriters (Goldman lead, Morgan Stanley and JPMorgan in syndicate) hold an option for an additional 83.3 million shares (the greenshoe). First trade on NASDAQ as SPCX is June 12.

What makes this offering atypical. The 30% retail allocation (~$22.5B) is the largest direct-to-retail carve-out any mega-IPO has ever extended, routed through Robinhood IPO Access, Fidelity, and Charles Schwab. (StockCram is not affiliated with any brokerage mentioned.) The lockup is not the standard 180-day cliff; it's a phased, tiered release tied to Q2 and Q3 earnings reports plus a rolling schedule at 70/90/105/120/135 days post-IPO. Musk himself is locked up for a full year with no early-release exceptions.

What bulls say (Wedbush's Dan Ives, PIMCO and BlackRock's published commentary): real revenue across launch contracts, Starlink ARPU, and post-xAI AI compute; NASDAQ-100 Fast Entry triggers mandatory passive buying within ~15 trading days of listing; broadest retail democratization in mega-IPO history.

What bears say (Morningstar most concretely): fair-value estimate of roughly $63/share against a $135 IPO price implies the offering is overvalued by about half. S&P Dow Jones declined to relax S&P 500 entry on June 4, blocking what Bloomberg Intelligence estimated would have been ~$14B of forced S&P-500 buying for SpaceX.

The disagreement isn't about whether SpaceX is a real, important, structurally diversified company; both sides agree on that. It's about whether the $1.75T price already reflects the risks the bears see, or leaves room for the growth the bulls expect.

Key Takeaway: The largest IPO on record priced tonight at $135. The non-standard elements, record retail allocation and staggered lockup, matter as much as the headline valuation.

SpaceX's first trading session is now complete. Here is what actually happened: the confirmed Day-One result, which supersedes the pre-trade expectations described in the mechanics sections below.

SPCX did not trade the instant the market opened. As is normal for an offering this size, NASDAQ first ran its opening price-discovery auction (the Cross) before any shares changed hands. The first official indications printed around 9:50 a.m. ET near $171–175, roughly 27–30% above the $135 IPO price, and the stock opened for trading shortly after, with the first public trade clearing near $150. That delayed open was the standard IPO auction process, not a sign of trouble and not an LULD volatility halt. (CBS News; NPR; 24/7 Wall St..)

From there SPCX ran higher, touched an intraday high of $176.52 (about +31% over the IPO price), then gave some of that back to close its first day at $160.95, up roughly 19% from the $135 IPO price. That put SpaceX's market capitalization at approximately $2.1 trillion, instantly among the most valuable U.S. companies and confirming the largest IPO on record by a wide margin, surpassing Saudi Aramco's 2019 debut.

What the Day-One print does and doesn't tell us. A first-day close above the IPO price means demand cleared at a premium on Day One: buyers at the open paid less than the intraday high but more than the $135 IPO allocation price, exactly the premium dynamic the retail-access section flagged. What it does not tell us is anything definitive about the next 30, 90, or 180 days. The durable questions are still ahead: NASDAQ-100 Fast Entry (~15 trading days out, an early-July window), the staggered lockup tranches running through late 2026, and whether 2025's $4.94B net loss narrows toward the profitability gate that keeps SPCX out of the S&P 500. Those are the signals tracked in the watchlist below. Historical data shown; past performance does not indicate future results.

Since the debut (as of late July 2026): After closing its first day at $160.95, SPCX peaked at $225.64 on June 16, then fell sharply. By mid-July it had dropped below its $135 IPO price, and on July 23 it set an all-time low of $110.85, trading near $113 on July 25, well below both its June peak (~$225) and its $135 IPO price. On July 7 it became the fastest company ever added to the NASDAQ-100 (about $4.3 billion of passive inflows), but the stock sold off into and after inclusion in a textbook 'sell the news.' The second-quarter report, now expected in early September, opens the first staggered lockup window. Historical data shown; past performance does not indicate future results. (CNBC, "SpaceX stock sinks below $135 IPO price", July 2026; Investing.com.)

Key Takeaway: SPCX opened near $150, peaked at $176.52, and closed its first day at $160.95, up about 19% over the $135 IPO price, at roughly a $2.1T valuation. It later ran to $225.64 on June 16, then fell below its $135 IPO price, trading near $113 by late July. The forward catalysts (NASDAQ-100 inclusion, the staggered lockup) still matter more than the Day-One print.

SpaceX bypassed the traditional price-range process entirely and went straight to a fixed $135 per share, itself a signal of book-building confidence, then confirmed that price after closing institutional orders on June 10. The final raise comes to $75 billion across roughly 556 million shares, putting SpaceX's IPO-day market capitalization at approximately $1.75 trillion. With the ~83 million-share greenshoe, the implied total proceeds if fully exercised approach $86 billion, which would push the record higher still.

The SEC documents disclosed in the public S-1 on May 20, 2026 showed SpaceX's full-year 2025 financials for the first time: revenue of $18.67 billion (up 33% year-over-year) and a net loss of $4.94 billion. The losses matter less for the IPO price than for the company's index-inclusion path, more on that below, and for how the bear case frames valuation.

The syndicate is top-tier. Goldman Sachs is the lead bookrunner; Morgan Stanley and JPMorgan Chase round out the lead positions, with a broader group of co-managers underneath. Reputable, full-strength bookrunning: the kind of syndicate that signals institutional comfort even before pricing.

What closed tonight was the institutional allocation. Tomorrow morning's open will tell us whether the heavy oversubscription (Bloomberg reported ~2× on June 8) translates into a sustained day-one premium or a more orderly tape; both are possible at this scale, and which one happens carries information about how durable the bid is.

Key Takeaway: Every confirmed number sits at the upper bound of what was reported in May. The institutional book held; whether retail demand at the open keeps that price tomorrow is the open question.

Confirmed numbers as of June 11, 2026 pricing.

| Value | Metric |

|---|---|

| SPCX | Ticker |

| NASDAQ | Exchange |

| June 12, 2026 | First trade |

| $135 / share (fixed) | IPO price |

| 555,555,555 | Shares offered |

| +83,333,333 shares | Greenshoe option |

| $75B (~$86B with greenshoe) | Total raise |

| ~$1.75T | IPO-day market cap |

| Goldman Sachs | Lead underwriter |

| Morgan Stanley, JPMorgan | Lead syndicate |

| ~30% (~$22.5B), record-largest | Retail allocation |

Quick framing before we go deeper. Like the wave overview, this article uses a three-tier confidence framework: public S-1 filings and the official pricing release are highest-confidence; numbers reported by credible journalists but not in primary documents are medium-confidence; rumors and forward-looking inferences are lowest-confidence. Treating them as equivalent is how readers get burned in fast-moving IPO coverage.

We'll cite each item with its strongest available source as we go through the piece.

Key Takeaway: The three-tier framework is most of the discipline. Trust the public S-1 and pricing release most, treat reported items as reasonable inference, treat rumors and forward-looking estimates as scenarios.

Three tiers of disclosure. Most pre-listing IPO writing mixes these together; we keep them separate.

| Items | Status |

|---|---|

| $135/share final pricing · 555,555,555 shares offered · 83.3M-share greenshoe · $75B raise · `SPCX` ticker · NASDAQ listing · June 12 first trade · Goldman/MS/JPM syndicate · 2025 financials ($18.67B rev, $4.94B net loss) · S&P Dow Jones June 4 decision not to relax S&P 500 entry rules · NASDAQ-100 Fast Entry rule effective May 1 · Staggered lockup schedule per S-1 disclosure · Musk's 1-year hold (no early-release exceptions) | Confirmed (public filings + official pricing release) |

| ~30% retail allocation (~$22.5B) (CNBC, NPR) · Institutional book ~2× oversubscribed (Bloomberg, June 8) · ~$150B total demand for $75B raise · Expected first-trade open above $135 · Multiple LULD trading halts would not be surprising given the size · ~$50B of cross-market selling pressure as institutions reposition · FTSE Russell fast-entry eligibility · Specific underwriter co-managers | Reported (credible journalism, not yet in primary documents) |

| Tesla-SpaceX merger (Dan Ives 80-90% odds; first half 2027 target) · Auto-trigger of Musk's $1T Tesla pay package on combined entity reaching $7.5T market cap · Morningstar's $63 fair-value estimate (analyst opinion, not official guidance) · Day-1 closing price · Lockup-expiration price action (path-dependent, see Meta 2012) | Rumored / inferred / forward-looking |

When a buyer hits the bid on SPCX tomorrow, they're buying a slice of a company that does not resemble the SpaceX of two years ago. The February 2026 all-stock absorption of xAI rolled Elon Musk's AI lab into SpaceX at a combined $1.25 trillion valuation ($1.0T SpaceX + $250B xAI). What now trades publicly is a launch + Starlink + AI infrastructure conglomerate, with all three businesses contributing to the revenue base. (CNBC, February 3, 2026.)

The revenue breakdown that bulls cite: launch contracts (commercial, NASA, DoD) provide the cash-generating foundation; Starlink subscriptions provide recurring ARPU that scales with the satellite constellation; the xAI compute and Grok-platform monetization layer in on top. Bears note that no comparable public company exists with this exact business mix, which makes peer-multiple comparison difficult: Lockheed Martin and Boeing are launch comparables but no Starlink, AT&T-style telecom is closer to Starlink but no launch, and AI labs like Anthropic are closer to xAI but no rockets. The closest synthetic comparable is a portfolio: roughly equal-weighted basket of Lockheed, AT&T, and Nvidia would approximate the integrated exposure. Whether that synthetic blend justifies $1.75T is exactly what bulls and bears are arguing.

For context on the wave as a whole, including where SpaceX sits versus Anthropic and OpenAI, our wave overview covers each company side-by-side.

Key Takeaway: SPCX is exposure to a conglomerate without a clean peer multiple. That's the source of the valuation argument.

The SpaceX stock ticker is SPCX, trading on NASDAQ starting June 12, 2026. Here's what's actually available to retail investors: at the IPO price, at the open, and after.

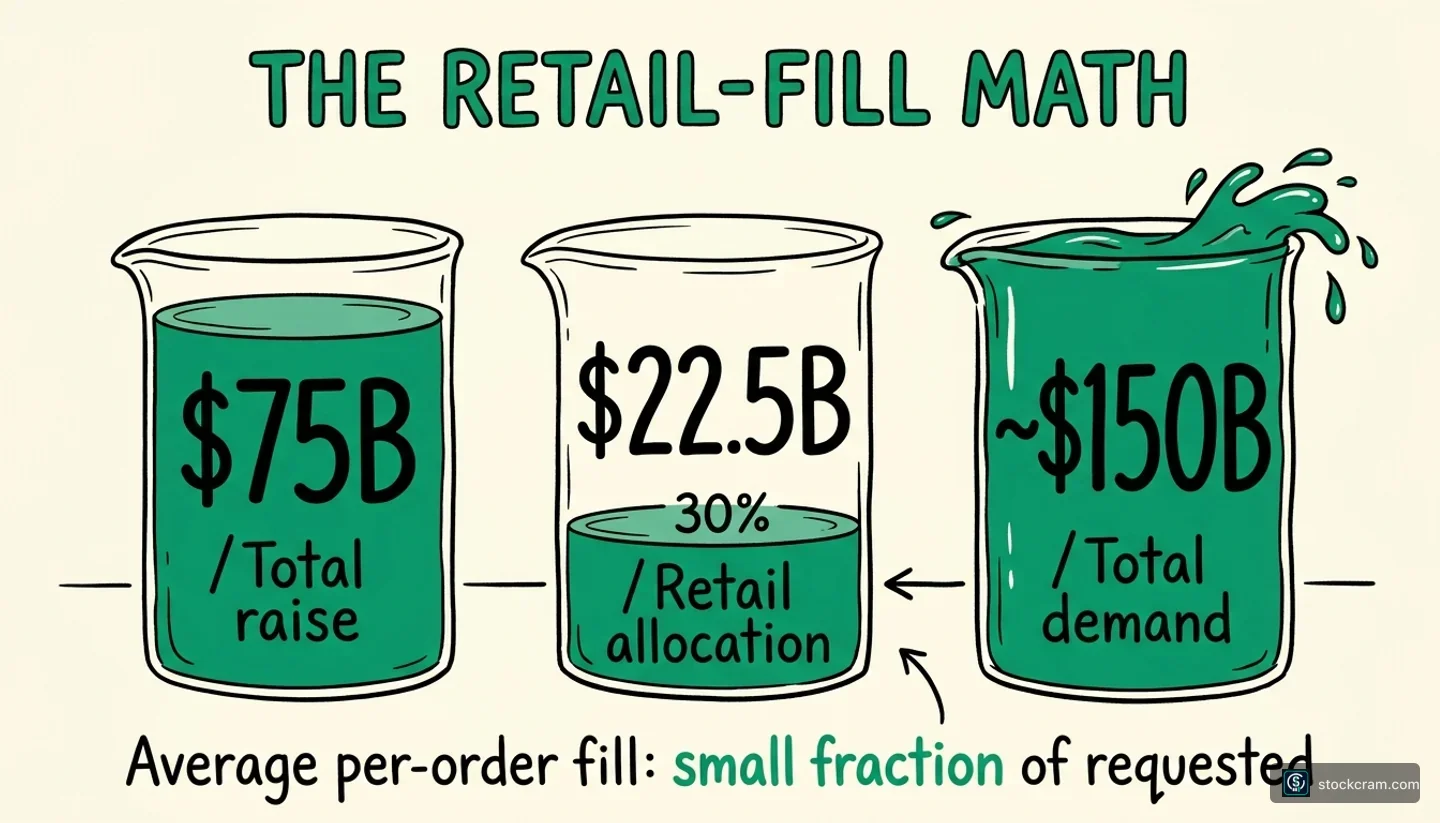

Headlines all week have been variations of "SpaceX is letting retail buy 30% of the IPO." That's directionally true. It's also an oversimplification of what the math actually says about your odds of getting filled.

The 30% retail allocation translates to roughly $22.5 billion of shares set aside for individual investors through three brokerages: Robinhood IPO Access, Fidelity, and Charles Schwab. (StockCram is not affiliated with any brokerage mentioned.) For mega-IPO context, that's enormous: typical retail allocation on a deal this size is 5-10%, so SpaceX's program is roughly three to six times larger than the historical norm.

But here is the math nobody is publishing. Bloomberg reported on June 8 that the institutional book was already ~2× oversubscribed: roughly $150B of demand against $75B of supply. Retail demand is almost certainly higher in number of orders even if smaller in dollar value. With retail allocation capped at ~$22.5B and demand likely to be a multiple of that even at modest per-account requests, average fill rates could be materially lower than requested allocations if retail demand resembles the institutional demand levels Bloomberg has reported. "Retail allocation available" is not the same thing as "every retail account that wants 100 shares will get 100 shares."

Visualized as three beakers, the gap between supply and demand is the whole story:

The 30% retail carve-out is real and historically large. The roughly 7× imbalance between total demand and retail allocation is the reason most retail submissions will be filled at a small fraction of requested.

Three practical paths exist for most readers, and they aren't equally available. The first is requesting shares at the IPO price through Robinhood, Fidelity, or Schwab IPO Access: eligibility varies by brokerage (minimum balances, account history, sometimes invitation-only access) and submission doesn't guarantee a fill. The second is buying on the open market on June 12 once SPCX trades; anyone with a brokerage account can buy at the market price, which may be materially above or below the $135 IPO price. The third, and arguably the simplest, is gaining exposure via index ETFs after inclusion: once SpaceX enters the NASDAQ-100 (~15 trading days after listing under Fast Entry), any NASDAQ-100 ETF such as QQQ gets weighted SPCX exposure automatically.

One caution on the open-market path. Multiple sell-side desks and at least one Morningstar piece have flagged that the open could come in well above $135, which means buyers at the open are paying a premium that IPO-price allocators didn't. Whether that premium holds or fades inside the first 30 days is itself path-dependent. We cover the Day-1 mechanic, including the LULD-halt rule that can pause trading on a volatile debut, in a later section.

None of the three paths is a recommendation. The map exists so readers can plan rather than panic-decide on listing day. Whether SPCX belongs in a specific portfolio depends on the portfolio, not on whether the headline is exciting.

Key Takeaway: Retail access is materially broader than any prior mega-IPO. The realistic per-order fill rate is still small. Simplest exposure for readers who want it is probably the post-inclusion NASDAQ-100 ETF route.

A debut at this scale is unusual to watch, and the cleanest way to read one is to know what happens mechanically before the headlines start firing. (For what actually happened on June 12, see the Day-One update above; this section explains the why behind it.)

The open is never at the IPO price. NASDAQ uses a price-discovery auction process, a Cross, for new listings, where institutional and retail orders interact to find an opening price that clears the most volume. The IPO price ($135) is what the underwriters allocated shares at the night before; the open is the first publicly tradeable price, and finding it takes time, which is why SPCX's first indications didn't print until mid-morning and the stock opened well above $135. How much of a premium the open carries is the first data point of any debut.

Halts are a built-in possibility, not a forecast. SPCX is subject to the same LULD (Limit Up-Limit Down) rules that apply to all NMS-listed stocks: automatic five-minute trading halts trigger when the price moves outside a defined band in a short window. On a volatile debut, one or more halts are always possible: potentially both up-halts (extreme upside moves) and down-halts (sharp pullbacks) within the same session. The key thing for beginners to understand is that a halt is not a sign of failure; it's the system working as designed to give the order book time to find equilibrium when prices move fast. (Note the difference from the opening-auction delay above: that delay is the normal price-discovery process, not a volatility halt.)

Three things matter most for reading a debut's tape. First, where the open clears versus the IPO price: that's the institutional-vs-retail demand snapshot. Second, the institutional-vs-retail volume mix in the first hour, which the tape reveals indirectly through the size distribution of trades. Third, whether the price closes above or below the open, which is the actual day-one signal sell-side desks write about afterward.

A reality check from prior mega-IPOs. Aramco (the closest size comp) opened roughly flat-to-down on its 2019 first day. Meta opened modestly above its $38 IPO price in May 2012, then closed near the IPO price, then cratered to $18 over the following four months. Alibaba popped 38% on its Day 1 in 2014 and held. There is no single playbook: even when a deal is broadly considered hot, what the first day means for the next 30/90/180 days is path-dependent. Historical data shown; past performance does not indicate future results.

Key Takeaway: The opening auction takes time and the open is always a premium-or-discount to the IPO price, not the IPO price itself. Halts are part of the design, not a sign of trouble. The signals worth watching are the open premium, the volume mix, and whether the close lands above or below the open.

Most IPO coverage focuses on what's likely to go right. The opposite framing is at least as useful for readers trying to understand a debut. Here are five scenarios that can meaningfully disrupt a mega-IPO's opening day, useful as a lens on June 12 and on the Anthropic and OpenAI debuts still to come, each with a brief note on what it actually looks like.

The open prints 40%+ above the IPO price. A blowout open above roughly $189 would be a strong-demand signal but also a Day-1 risk for retail buyers who bought the open. Mega-IPO openings that print far above the IPO price have, historically, often given back a meaningful chunk of that premium over the following days as the institutional book unwinds. Alibaba opened 38% above its IPO price in 2014 and held; Snap opened 41% above its 2017 IPO price and was below the open within months. Path-dependent.

The retail allocation comes in lower than the headline 30%. Underwriters retain discretion to reduce the retail tranche if the institutional book is strong enough to absorb more supply at the IPO price. If retail allocation ends up at 20% rather than 30%, fill rates per submitted order would compress further, and any retail buyer who built a thesis around the "democratized IPO" framing would have to reconsider.

Heavy profit-taking inside the first hour. With an unusually large retail allocation and an oversubscribed institutional book, the open is likely to contain a mix of long-term holders and short-term profit-takers. If the latter dominate the early tape, SPCX could see down-halts within the first 30-60 minutes regardless of underlying demand. That dynamic has historically been the single most common Day-1 negative signal.

A market-wide risk-off move. SPCX's open coincides with whatever else is happening macro-wise on June 12. A broad equity selloff (rates spike, geopolitical shock, surprise inflation print) on the same day would compress the IPO premium independent of SpaceX-specific demand. Worth checking the broader tape before drawing conclusions from the SPCX print.

Underwriter stabilization activity. Underwriters typically have the option to support the share price in the first 30 days post-IPO through stabilizing bids and the greenshoe mechanism. If you see SPCX hold a tight range near the IPO price despite weak retail demand, stabilization may be the reason, not organic interest. The pattern usually shows up as repeated buying at round-number price levels and a noticeably tighter spread than market depth would justify.

None of these scenarios is a prediction. They're a checklist for distinguishing real Day-1 signals from noise.

Key Takeaway: Use this list to distinguish genuine signal from noise tomorrow. A halt is mechanics; a heavy profit-taking wave inside hour one is the most common Day-1 negative signal.

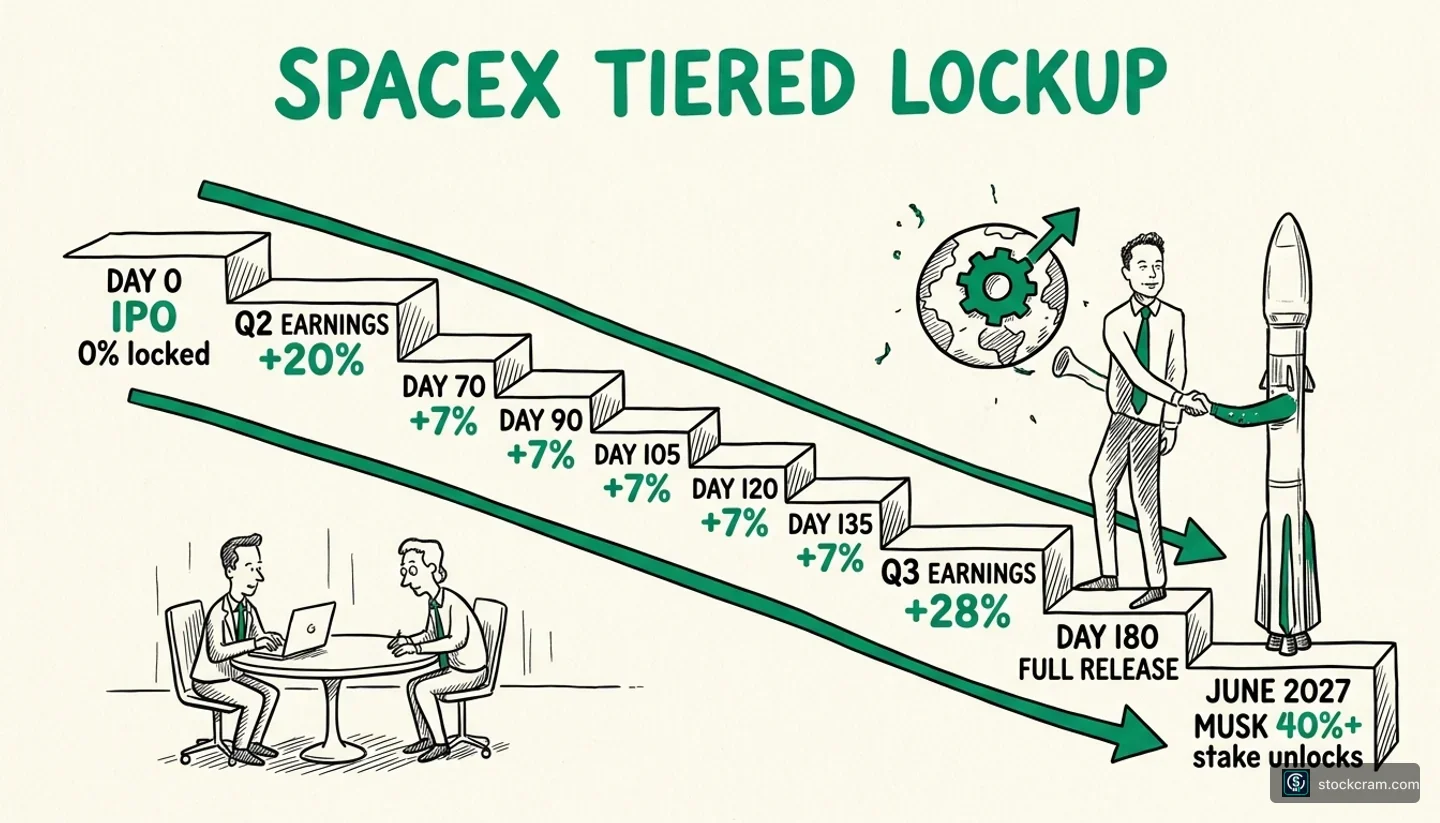

Most coverage you'll see this weekend will say SpaceX has a "standard 180-day lockup." That's wrong. The S-1 disclosed a staggered, multi-tier release schedule unlike the typical mega-IPO cliff, and it matters because it changes both the timing and the concentration of post-IPO insider selling pressure.

Here is what the filing actually says. After SpaceX reports earnings for Q2 2026 (the three months through June), now expected around September 2, 2026, the first release window opens: roughly 911.5 million shares (about 6.97% of shares outstanding), with a $175.50 five-day price trigger that could free roughly another 455.8 million shares. From there, a rolling release at 70, 90, 105, 120, and 135 days post-IPO allows another 7% at each interval. After SpaceX reports Q3 2026 earnings (the three months through September), an additional 28% becomes sellable. At the 180-day mark, whatever remains is fully released. (CNBC, May 21, 2026; Morningstar coverage of the tiered structure.)

Musk is a separate, stricter case. The S-1 carves him out of every early-release provision. His ~40%+ stake is locked up for a full year from the IPO date, to June 2027, with no exceptions. That's a deliberate signal of long-term commitment, and bulls cite it as a tail-risk reducer.

Why this structure matters. The traditional 180-day cliff concentrates all eligible insider supply on a single day, which is why so much pre-IPO commentary fixates on the lockup date. By spreading SpaceX's release across two earnings windows and a rolling 70-135 day schedule, the supply hits the market in smaller batches over four to five months, which (in theory) lets the market absorb each tranche without a one-day crash. Whether that smoothing actually works is the test the next six months will run.

Visualized as a staircase descending from Day 0 to Musk's June 2027 release, the schedule reads less like a cliff and more like a controlled release:

Most pre-IPO commentary focuses on a single 180-day cliff date. SpaceX's design spreads supply across 9 separate release events over 12 months: the deliberate smoothing is what makes this lockup structurally novel.

The biggest pre-IPO investors who become eligible to sell across this schedule are Founders Fund (Peter Thiel's, from a $20M Series C in 2008), Sequoia Capital, Alphabet (through Google's 2015 investment), and Fidelity. Their reactions to each tranche release will be one of the most-watched signals of late 2026, and the eventual deep-dive on the December lockup-expiration window is one we'll cover separately as it gets closer.

Key Takeaway: The staggered structure is unusual by IPO standards and tries to engineer away the cliff-edge selloff. Whether the smoothing works is one of the most-watched stories of the next six months.

Approximate timing based on the S-1 disclosures. Specific dates depend on when SpaceX reports earnings.

| Trigger | Released | Milestone |

|---|---|---|

| First trade June 12, 2026 | 0% (all locked) | Day 0, IPO |

| First public earnings report | ~6.97% (~911.5M shares); +455.8M if $175.50 5-day trigger hit | ~Sep 2026, Q2 earnings |

| Calendar-based | +7% | Day 70 |

| Calendar-based | +7% | Day 90 |

| Calendar-based | +7% | Day 105 |

| Calendar-based | +7% | Day 120 |

| Calendar-based | +7% | Day 135 |

| Second public earnings report | +28% | ~Nov 2026, Q3 earnings |

| Standard lockup expiration | Remaining balance fully released | Day 180, Dec 2026 |

| Musk's hold ends | Musk eligible to sell (40%+ stake) | June 2027, Day 365 |

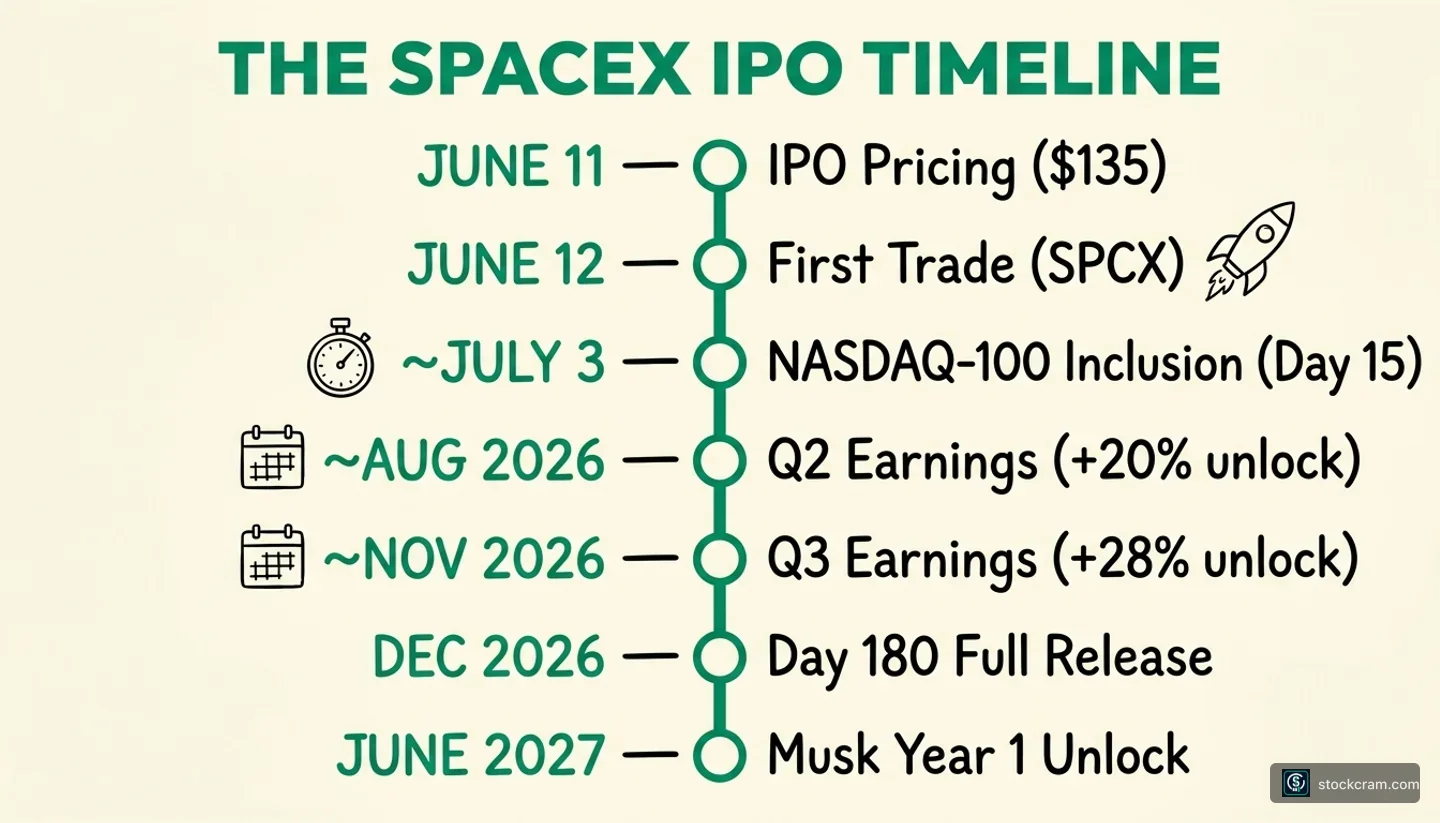

Putting the index-inclusion, lockup, and Musk-specific milestones on a single timeline makes the next 12 months easier to plan around.

Seven milestones, from pricing tonight through Musk's June 2027 unlock:

The seven dates above are the framework most worth bookmarking: bull or bear, every meaningful catalyst for SPCX between now and mid-2027 sits on this stack.

Key Takeaway: Track these seven dates rather than the daily SPCX print. Every meaningful change in the supply/demand picture sits on this timeline.

Two of the three major U.S. index families said yes to fast-tracking SpaceX. One said no. The split matters because it determines how much mechanical, mandatory passive-fund buying SPCX will draw inside the first 30 days versus the first 18 months.

The NASDAQ-100 mechanic stands. On May 1, 2026 NASDAQ implemented its Fast Entry rule: newly listed top-40-by-market-cap names enter the NDX after just 15 trading days of seasoning, down from approximately six months previously. SpaceX, listing as the largest U.S. company by market cap, easily clears the top-40 bar. Roughly 15 trading days after June 12, every passive fund tracking the NASDAQ-100 (QQQ being the largest, but a wide range of other trackers too) is required to buy SpaceX. The estimated mechanical buying via NASDAQ-100 alone is in the low-to-mid double-digit billions.

FTSE Russell took the same path. They announced parallel fast-entry rules in May 2026, and SpaceX is now eligible for inclusion in both the Russell US Equity Indexes and the FTSE Global Equity Index Series. The additional mechanical buying from FTSE-tracking funds is smaller than NASDAQ-100 but not trivial: a few additional billion in forced demand on top of the NASDAQ-100 bid.

S&P Dow Jones went the other way. After a public consultation, on June 4, 2026 the index committee confirmed it would not relax the S&P 500's existing requirements (GAAP profitability, 12-month seasoning, investible-weight-factor minimums). SpaceX, with $4.94B in 2025 net losses, cannot be added to the S&P 500 until it both becomes GAAP-profitable and clears the seasoning window: earliest mid-2027, and only if profitability arrives by then. Bloomberg Intelligence estimated that S&P fast inclusion would have driven roughly $14 billion of forced passive buying for SpaceX alone. That bid does not happen.

What to expect over the next 30 trading days. NASDAQ-100 inclusion typically triggers about 15 trading days after IPO if all other criteria are met: for SpaceX that fell on July 7, 2026, when it became the fastest company ever added to the NASDAQ-100. FTSE Russell additions follow their own quarterly review schedule. S&P 500 inclusion is off the table for at least a year regardless of how SPCX trades.

Key Takeaway: Two of three index families said yes. The bigger one, S&P 500, said no. The forced mechanical bid is real but smaller than it would have been if S&P had relaxed rules.

This section is explicitly forward-looking and speculative. Treat what follows as material rumor with a credible analyst chorus behind it, not as a near-term certainty.

Wedbush's Dan Ives is the most prominent analyst publicly modeling a combination. His current probability assessment is 80-90% for a merger completed in the first half of 2027, up from his initial "80%" framing in late May (Yahoo Finance; TheStreet). Ives' framing is that the combination would create a single Musk-controlled entity spanning rockets, satellites, EVs, energy storage, and AI infrastructure: combined market cap somewhere between $3.4T and $3.6T depending on Tesla's trading level.

What makes the timing material rather than abstract is the pay-package mechanic. Per Electrek's reading of the Tesla compensation terms, a SpaceX-Tesla combination could automatically trigger Musk's $1 trillion CEO pay package by accelerating the combined entity past the $7.5T market-cap milestone, meaning compensation tied entirely to market-cap performance rather than operational milestones. That creates a real CEO incentive to consummate the combination on Ives' timeline rather than let SPCX trade independently for years. Fortune (June 4) also flagged a single sentence in SpaceX's amended S-1 about issuing significant equity in future transactions as too pointed to be boilerplate.

None of this is confirmation. Musk has made no on-the-record statement. Neither board has acknowledged anything publicly. Bulls treat the merger as upside optionality on SPCX; bears treat it as execution complexity for the next 12-18 months that adds variance regardless of direction. The honest read is that the conversation is real and worth bookmarking, and that any rebalancing of position size around it should wait for a confirming signal from Musk or the boards.

Key Takeaway: The merger is unconfirmed but the analyst consensus, pay-package incentive, and S-1 language all point the same direction. Treat it as material rumor, not certainty, and watch for Musk statements or board disclosures in the coming weeks.

The bull case for SpaceX at $1.75T has named voices and concrete arguments. Stripping out the noise, the strongest version of it rests on five pillars.

First, diversified revenue with multiple growth vectors. Launch contracts (commercial, NASA, DoD) provide the cash-generating foundation that traditional space companies have always had. Starlink subscriptions add ARPU that scales with the constellation buildout, a recurring revenue base that grows whether the broader market is bullish or bearish on AI. The post-xAI compute layer adds AI infrastructure exposure during a hyperscaler-capex cycle that is itself running at $700B+ in 2026 (covered in detail in our AI bubble piece). The diversification means SPCX is not a single-thesis bet.

Second, structural rule changes that recognize the company's market-cap weight. NASDAQ-100 Fast Entry and FTSE Russell's parallel inclusion provide mandatory passive demand in the low-to-mid double-digit billions within the first 30 days. Bulls treat this as a methodology fix overdue for the era of long-private companies, not artificial pumping.

Third, the staggered lockup as a stability feature. The non-standard tiered release was designed to smooth post-IPO selling pressure rather than concentrate it on one day. If the smoothing works, SPCX avoids the one-day cliff selloff that has hurt prior mega-IPOs (Meta's first lockup, for instance, drove the stock to its $18 post-IPO low). Bulls cite this as a structural improvement over the standard playbook.

Fourth, named institutional commentary. PIMCO's and BlackRock's June commentary (collated by TradingKey) is bullish on the AI infrastructure capex cycle that SpaceX-via-xAI now sits inside. When two of the world's largest asset managers tell clients to expect continued acceleration, the active money is broadly aligned with the wave rather than fighting it. Ives' "opening of the floodgates" framing is consistent across his Wedbush notes.

Fifth, retail-democratization optionality. The 30% retail carve-out is structural rather than marketing: it's the first time U.S. retail investors get direct IPO-price access to a trillion-dollar private-tech name at this scale. Bulls argue that broadens long-term ownership distribution in ways that historically reduce volatility once the dust settles.

None of these are absolute. Each has a counter the bears press on, which is the next section.

Key Takeaway: Bulls aren't arguing SpaceX is small or unprofitable forever. They're arguing the diversification, structural rule changes, and lockup design make $1.75T defensible, and that the wave's mechanical bid will reinforce it.

The bear case has its own named voices and dated data points. The strongest version isn't "SpaceX is fake." It's that timing, valuation math, and historical precedent all point in the same direction.

The cleanest single bear data point comes from Morningstar. In their pre-IPO assessment, Morningstar published a fair-value estimate of roughly $63 per share, a 53% discount to the $135 IPO price, implying the offering is overvalued by approximately half. At the company level, that translates to a $780 billion fair-value estimate against the $1.75 trillion IPO valuation. Morningstar analyst Nicolas Owens's discounted cash flow model values the combined launch and Starlink satellite businesses at about $611 billion in enterprise value, plus another $170 billion in probability-weighted scenarios for the company's AI operations. (CNBC, June 3, 2026; Yahoo Finance summary.) Fair-value estimates from independent research desks are analyst opinion, not official guidance, but Morningstar's methodology is well-documented, and the headline framing they used ("significantly overvalued") is direct enough that it's worth taking on its own terms whether you agree or not. The comparison to Aramco below is useful for IPO-scale analysis, not business-model comparison.

The structural pattern bears cite. Mega-IPOs concentrated near market tops have a track record. Saudi Aramco IPO'd in December 2019 at $1.7T, ran flat-to-down on Day 1, and over the six years since has returned roughly +15% while the S&P 500 returned over +100% and sector peers (Exxon, Chevron, Shell, Total) all returned 55-65%. Being the biggest IPO does not make a stock the best buy.

The valuation math, bear flavor. At $1.75T market cap and roughly $19B in 2025 revenue, SPCX is trading at approximately 92× revenue. For context: Nvidia trades around 25× sales; Lockheed Martin around 2×; AT&T around 1.5×. Bulls counter that revenue is the wrong multiple, that adjusting for growth potential and recurring Starlink ARPU you get to a more defensible number. Bears respond that 92× sales at a $4.94B loss is the kind of multiple that requires perfect execution for years to grow into.

The S&P 500 denial as a real-world bear data point. The June 4 S&P Dow Jones decision to maintain existing rules, refusing to relax profitability and seasoning requirements, stripped what Bloomberg Intelligence estimated would have been ~$14B of forced S&P-500 buying for SpaceX in its first year. That's a quantifiable demand headwind that didn't exist two weeks ago, and it constrains the index-mechanic tailwind to NASDAQ-100 and FTSE Russell only.

The lockup-expiration cluster. Even with the staggered structure designed to smooth supply, the cumulative tranche releases through November-December 2026 represent the largest pre-IPO equity overhang in market history. Founders Fund's 2008 Series C position has appreciated roughly 62,000% at current valuations; even a partial exit creates meaningful supply. Whether the smoothing absorbs that supply orderly is one of the bear case's main watchlist items.

Key Takeaway: Bears aren't arguing SpaceX won't be important. They're arguing $1.75T leaves no margin for execution risk, and that the historical mega-IPO pattern plus Morningstar's DCF point in the same direction.

History suggests both sides might be right at different time horizons, measuring different things on different clocks.

The Cisco parallel is the cleanest illustration. Cisco was the dominant, profitable infrastructure company at the heart of the internet revolution. Bulls in 1999 were correct that Cisco would matter for decades. Bears in 1999 were also correct that Cisco's stock would fall about 85% from its 2000 peak. Both facts coexisted, and a buyer who believed both could have positioned around either thesis at different points in the timeline.

The Aramco parallel is the cleanest illustration for SpaceX specifically. Aramco is a real company that pumps real oil and generates real cash. It was the biggest IPO in history at the time. It also materially underperformed the S&P 500 over six years. The company is structurally important. The stock was a poor buy at IPO. Neither claim cancels the other.

If that's how SPCX resolves, the most likely outcome is that SpaceX remains a structurally important company and delivers disappointing 5-year stock returns relative to the S&P 500. Morningstar's $63 fair-value estimate could be right about prices in the next few years; Ives' merger thesis and PIMCO's AI-capex framing could be right about long-term importance. The two views aren't actually in conflict; they're measuring different things on different timelines.

That's not a comforting framing. It's just the historically most common one when a real innovation meets an enthusiastic market.

Key Takeaway: A real revolution can produce real winners and still produce dramatic stock losses for buyers who paid too much. 'Both sides right' is historically more common than 'one side right' for IPOs at this scale.

Each side has concrete signals over the next twelve months. The list below is the framework we'd recommend bookmarking: these are the events that will move the debate, not the daily price action.

Key Takeaway: Watching the staggered lockup tranches and the index-inclusion mechanic is more informative than watching daily SPCX price action.

Bookmark this and check back each week. Same signals serve both bull and bear analyses.

| Signal | Bears Watch | Bulls Watch |

|---|---|---|

| Day-1 open vs $135 | Open below or near $135, soft retail demand | Open materially above $135, strong institutional + retail bid |

| First-week LULD halts | Repeated down-halts on profit-taking pressure | Up-halts driven by retail demand exceeding allocation |

| ~Day 15 NASDAQ-100 inclusion | Inclusion priced in, no mechanical bump | Mandatory passive bid drives clean step-function up |

| Q2 2026 earnings (~Sep) | Revenue miss + first 20% insider unlock = supply cliff | Revenue beat + orderly absorption of 20% tranche |

| Q3 2026 earnings (~Nov) | Bigger 28% unlock + any guidance cut = pressure | Earnings strength + smoothed absorption |

| 180-day full release (~Dec) | Remaining-share cliff selloff | Most supply already absorbed via earlier tranches |

| Tesla-merger confirmation | Merger collapses → SpaceX standalone re-rate lower | Merger confirmed → combined entity premium expands |

| Musk public statements | No long-term commitment messaging | Reinforces 1-year hold + standalone-vs-merger clarity |

Five common misreads. None are dumb questions; they're the questions the headlines invite.

"Day-1 buyers get the IPO price." No. The IPO price ($135) is what underwriters allocated shares at to institutional and retail-program participants. Day-1 buyers buy at the market open, which for SPCX is being formed through NASDAQ's price-discovery auction. The open could be materially above $135, meaning Day-1 buyers pay a premium IPO allocators didn't.

"Trading halts mean the stock is in trouble." No. LULD (Limit Up-Limit Down) halts are automatic five-minute pauses designed to let order books find equilibrium when prices move fast. On a volatile mega-IPO debut, one or more halts are always possible: both up-halts (extreme upside) and down-halts (sharp pullbacks). They're a feature, not a failure. (Separately, the delayed open on a big IPO is the normal price-discovery auction, not a halt.)

"Lockup expiration always crushes the stock." Sometimes. The standard 180-day cliff has crushed some IPOs (Meta hit its post-IPO low at its first lockup release in 2012) and rallied others (Meta's biggest lockup, in November 2012, saw the stock rally +10% on the day). Path-dependent. SpaceX's staggered design is specifically built to avoid the cliff dynamic.

"The bigger the IPO, the better the stock." Aramco was the biggest IPO in modern history before SpaceX. It underperformed the S&P 500 by roughly 4× over the next six years. Size attracts attention; quality is a separate question.

"NASDAQ-100 inclusion guarantees gains." Mostly tailwind, but not magic. Tesla rallied ~70% after its December 2020 S&P 500 inclusion with $51B of mechanical buying behind it. But Snowflake and DoorDash both underperformed in the year following their NASDAQ-100 additions. The mechanical bid is real; everything else is up to the underlying fundamentals.

Key Takeaway: Most beginner confusion about a debut like SPCX's comes from treating the IPO price as the buy price and treating halts (or a delayed open) as trouble. All are normal.

Quick answers to the questions readers ask most about SPCX.

Selected primary sources for the figures, dates, and quotes in this article. Links go to publication homepages and verified primary documents; specific article URLs are described inline so readers can search them directly.

SpaceX filings and official pricing

Lockup structure and insider mechanics

Index inclusion

Bull and bear analyst voices

Tesla-merger and Musk pay package

Historical mega-IPO comparisons

Last reviewed: July 26, 2026 (updated through July 25 trading).

The pricing held at the high end of expectations.

$135/share on 555.6M shares for a $75B raise, the largest IPO in U.S. history. Greenshoe takes it to ~$86B if fully exercised.

The staggered lockup is the structural feature most coverage will miss.

Not a 180-day cliff. Earnings-tied releases at Q2 and Q3 plus rolling 70/90/105/120/135-day intervals. Designed to smooth, not concentrate, post-IPO selling.

The retail allocation is real but oversold in the headlines.

30% set aside (~$22.5B) is the largest retail carve-out in mega-IPO history. But demand likely dwarfs that, so per-order fills will be small.

Two of three index families said yes; the biggest said no.

NASDAQ-100 Fast Entry triggers ~15 trading days after listing. FTSE Russell adopted parallel rules. S&P 500 declined June 4: SpaceX blocked until at least mid-2027 (GAAP profitability gate).

Bears have a concrete fair-value number to point at.

Morningstar's roughly $63/share fair-value estimate against $135 IPO price implies the offering is overvalued by approximately half. Cite-able and dated.

The Tesla-merger conversation is material rumor, not noise.

Wedbush's Dan Ives at 80-90% probability for first-half 2027. Could auto-trigger Musk's $1T pay package via $7.5T market-cap milestone. S-1 language consistent with the thesis. Still unconfirmed.

Robinhood agentic trading lets an AI agent place trades in a dedicated, funded account. A calm, plain-English walkthrough of how it works and the risks.

A war headline turned your portfolio red and your finger is over the sell button. Here is a calm, educational look at panic selling and how to tell a reaction from a plan.

Is the housing market crashing in 2026? The truer answer: it's frozen, not crashing. The lock-in effect, both sides, in plain English.

SPCX is the NASDAQ ticker for SpaceX. First trade was June 12, 2026 on NASDAQ. The IPO price was set at $135 per share on the evening of June 11.

For most retail investors, you typically don't get the IPO price. Allocation goes to institutional clients of the underwriters (Goldman Sachs, Morgan Stanley, JPMorgan). SpaceX's unusual 30% retail carve-out runs through Robinhood IPO Access, Fidelity's IPO program, and Charles Schwab, but submission doesn't guarantee a fill, and average fill per order will likely be a small fraction of requested. *(StockCram is not affiliated with any brokerage mentioned.)* The practical retail path was buying at the open on June 12, which opened near $150, above the $135 IPO price.

Nobody can answer that without understanding your goals, time horizon, and risk tolerance, and you should be skeptical of anyone who answers it confidently. What investors typically do when uncertain about a mega-IPO Day 1: review position sizing (would this be 1% or 10% of your portfolio?), check whether the valuation multiple is defensible at any reasonable assumed growth rate, and consider whether you would be comfortable holding through a 50% drawdown without panic-selling. At its $135 IPO price SPCX traded at roughly 92× 2025 revenue, at the high end of even high-growth peers. Morningstar's fair-value estimate is roughly $63/share. Tools that help: our P/E ratio calculator, the Foundations course.

Generally yes, once SPCX is publicly traded on NASDAQ starting June 12, 2026. Any brokerage-enabled retirement account, a self-directed 401(k), Traditional IRA, Roth IRA, SEP IRA, or taxable brokerage account, can typically purchase shares from the open market, subject to your specific plan's restrictions on individual-stock trading. Two practical notes. First, employer-sponsored 401(k)s often limit holdings to a curated list of mutual funds and target-date funds; if SPCX isn't on your plan's menu, you can't buy it directly within that account, but you may be able to buy a NASDAQ-100 ETF (such as QQQ) that will include SPCX after Fast Entry inclusion (~15 trading days post-IPO). Second, IRAs at major brokerages (Fidelity, Schwab, Vanguard, etc.) generally allow individual stock trading, so an IRA is usually the more flexible retirement-account path for SPCX. *(StockCram is not affiliated with any brokerage mentioned.)* Check with your plan administrator for specifics.

There isn't a single expiration date: SpaceX has a staggered structure. The first release window, roughly 911.5 million shares (about 6.97% of shares outstanding), opens after SpaceX's Q2 2026 earnings, now expected around September 2, 2026; a $175.50 five-day price trigger could free roughly another 455.8 million shares. Another 7% releases at each of 70/90/105/120/135 days post-IPO. After Q3 2026 earnings (~November), an additional 28% releases. At Day 180 (~December 2026), whatever remains is fully released. Musk is locked up for a full year: he can't sell until approximately June 2027, with no early-release exceptions.

S&P Dow Jones announced on June 4, 2026 that it would not relax its existing rules, which require GAAP profitability and 12-month seasoning. SpaceX reported a $4.94B net loss in 2025, so it doesn't meet the profitability gate. Earliest possible S&P 500 inclusion is mid-2027, and only if SpaceX achieves GAAP profitability by then. SpaceX *is* eligible for the NASDAQ-100 (Fast Entry rule effective May 1, 2026) and FTSE Russell indices, where the rules were relaxed.

It's a serious analyst conversation but not confirmed. Wedbush's Dan Ives puts the probability at 80-90%, with first-half 2027 as the target completion window. Per Electrek's reading of the Tesla compensation plan, a merger could automatically trigger Musk's $1 trillion CEO pay package. Fortune (June 4) reported that a single sentence in SpaceX's amended S-1, about issuing significant equity in future transactions, reads as too pointed to be boilerplate. None of this is confirmation. Musk has made no on-the-record statement. Treat as material rumor, not certainty.

The standard 180-day cliff concentrates all eligible insider supply on a single day, which has historically created sharp post-lockup selloffs (Meta hit its post-IPO low at its first lockup release in 2012). SpaceX's design spreads supply across two earnings windows and rolling 70-135 day intervals, so the market absorbs each tranche in smaller batches over four to five months. The intent is to smooth supply rather than concentrate it. Whether it works in practice is one of the most-watched stories of the next six months.

Honestly, we'll know in hindsight. Bears (Morningstar, who put fair value at roughly $63 vs $135 IPO) argue $1.75T leaves no margin for execution risk. Bulls (Wedbush, PIMCO, BlackRock) argue diversified revenue across launch + Starlink + xAI compute makes the valuation defensible. Both sides cite real data. The historically most common outcome for mega-IPOs of this scale is that the company remains important AND the stock disappoints relative to the S&P 500 over the next five years. That's not a comforting framing; it's just what the Aramco / Cisco / Meta pattern suggests.