Is the Housing Market Crashing in 2026? Why It Feels Frozen Instead

Is the housing market crashing in 2026? The truer answer: it's frozen, not crashing. The lock-in effect, both sides, in plain English.

21 min read

Read Article

A war headline turned your portfolio red and your finger is over the sell button. Here is a calm, educational look at panic selling and how to tell a reaction from a plan.

Educational purposes only. This content does not constitute investment advice. Read our disclaimer

StockCram is not a broker-dealer, investment adviser, or financial institution. All content is for educational and informational purposes only and should not be construed as personalized investment advice. Consult a qualified financial professional before making investment decisions. Past performance does not guarantee future results.

You opened your brokerage app, saw a wall of red, and one question started looping: should I sell stocks during war? Maybe a Strait of Hormuz headline just crossed your feed, maybe a friend already moved everything to cash. Your heart rate is up and your finger is hovering over the sell button. That feeling is real and common. It is also a bad setup for a rushed decision.

This page will not tell you to sell or to hold. It will help you slow down, check whether your plan actually changed, and avoid turning a scary headline into a rushed trade. Along the way it separates a panic reaction from a planned decision and puts a few past war shocks in perspective. Nothing here is a recommendation to buy, sell, or hold, and none of it is a forecast.

It sits alongside our other Market Explainers guides on the mechanics of war and markets, so this page can stay in one lane: your reaction to the headline. You cannot control the war. You can control whether you trade before you have thought it through.

The short answer is that this is a planning question, not a yes-or-no question, and treating it like one is how people get hurt. Whether selling makes sense for you depends on things this article cannot see: when you need the money, how the rest of your money is arranged, and whether anything about your actual situation changed today. A war headline changes the news. It does not automatically change your financial plan.

So here is the reframe to keep in your head every time a scary headline hits: did the headline change my plan, or did it only change how I feel? Those are different events. A changed plan (you suddenly need cash next month, or your goals genuinely shifted) is a reason to make deliberate adjustments. A changed feeling is a mood, and moods make a poor basis for permanent moves. Volatility is uncomfortable, but discomfort is not new information.

We will not tell you to sell, and we will not tell you to hold. We will help you notice which of those two things actually happened, because that is the part you control.

News snapshot: US-Iran re-escalation, mid-July 2026. This is the kind of headline that sends people to a page like this. As reported (Reuters and AP, July 13-14, 2026), an interim US-Iran ceasefire collapsed in early July, the US resumed strikes on Iranian military targets, and Iran attacked shipping in the Strait of Hormuz and declared the waterway closed. President Trump ordered a renewed US naval blockade of Iranian ports, reported to take effect July 14, and floated, then walked back, a 20% fee on cargo through the strait. Markets moved the way they often do on a supply scare: U.S. stocks slipped on July 13, 2026, with the S&P 500 down about 0.8%, the Dow down about 0.3%, and the Nasdaq down about 1.6%, while Brent crude jumped nearly 10% to settle near $83 and kept climbing on July 14 (AP, Reuters). The episode appears here as an example of how war headlines stir portfolio anxiety, not as a forecast. This article does not predict the conflict; details are reported and evolving.

Key Takeaway: We cannot tell you whether to sell. We can help you tell whether the headline changed your plan or only your mood, because that is the part you control.

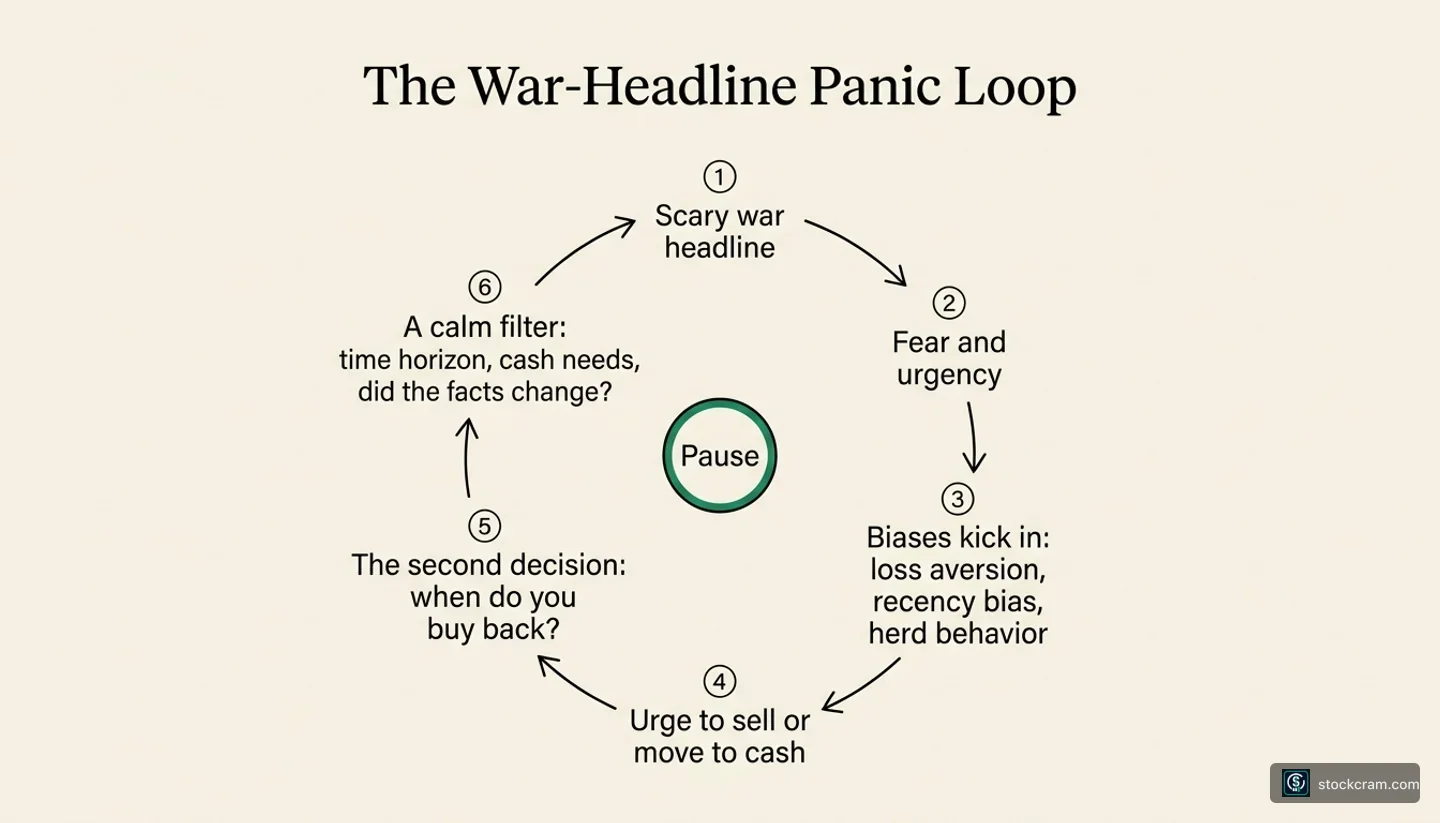

The urge to sell during a war scare is not a character flaw. It is a predictable output of how brains handle fear and money, and understanding the loop is the first step to noticing when you are inside it.

It usually runs like this. A breaking headline lands. Your body reacts before your reasoning does: heart rate up, attention narrowed, a sense that you must do something now. Then a few well-documented biases switch on and push you toward the sell button.

Loss aversion. Loss aversion is the finding that losses hurt roughly twice as much as equal gains feel good. A 10% drop does not register as the mild wobble a 10% gain would; it registers as pain, and the brain wants the pain to stop. Selling promises to stop it immediately. The catch is that the move which relieves the feeling fastest can be very different from the one that fits your plan.

Recency bias. Recency bias is the tendency to weight what just happened far more heavily than the long record. After a red day driven by a war headline, the last few hours feel like the whole story, and it is easy to stretch today's drop into tomorrow's crash. They rarely tell the whole story.

Herd behavior. Herd behavior is the pull to do what everyone around you is doing. When your feed, your group chat, and financial TV all lean one way, staying put feels reckless and joining the stampede feels safe. Fear is socially contagious, and a war headline is about as contagious as news gets.

Stack those three on top of market sentiment turning sour and you get a specific urge: sell, go to cash, or at least refresh the portfolio for the tenth time. That is panic selling, selling driven by emotion and the crowd rather than by any change in your own situation.

Put together, the sequence runs as a loop, each stage feeding the next:

Trace that loop for a moment, and notice what it never includes: a single new fact about the companies you own. None of those three forces is information about your finances. Loss aversion is about how loss feels. Recency bias is about how the timeline feels. Herd behavior is about how other people are acting. A war can genuinely matter to markets, and we are not waving that away. But the loop pushing your finger toward the button is made of feeling and social pressure, not of any fact about when you need your money. Naming the loop is how you buy a beat of space between the headline and the trade.

Key Takeaway: The panic loop is built from loss aversion, recency bias, and herd behavior. Naming it buys you a beat of space between the headline and the trade.

History will not tell you what happens next. What the record can do is loosen the grip of the assumption doing most of the damage right now: that war equals a permanent crash. The real picture is messier, and calmer, than that.

We are keeping this to one compact table on purpose. The full war-by-war account, with recovery times and sector detail, lives in our 80 years of stock-market data across major wars guide. Read the numbers as behavioral evidence, not a forecast.

Historical data shown; figures are approximate and vary by source; Historical data is context, not a forecast.

A few things stand out. In the first three cases (the Cuban Missile Crisis in 1962, the 1990–91 Gulf War, and 9/11 in 2001), the initial drop was real, but the market was higher ninety days later than at the shock. That is the pattern people mean when they say markets are resilient.

The fourth row keeps this honest. The 1973 Arab Oil Embargo was not a quick dip: stocks fell about 16% and were still down about 13% ninety days later, and the surrounding bear market took years, not months, to recover. The difference is worth understanding. A shock tied to a lasting hit to the real economy, an actual oil supply cut feeding a recession, has behaved very differently from a shock that was mostly a spike of fear. Some war-era selloffs took years to come back. Figures throughout are approximate and vary by source and methodology (Citi/Citigroup).

There is also a recent data point about behavior rather than prices. During the early 2026 Iran conflict, Vanguard reported that the S&P 500 fell about 9% from January 27 to March 30, 2026, then reached a record high by April 15, 2026. More telling: over the conflict window Vanguard measured, February 28 to April 8, 2026, only about 14% of Vanguard retail investors traded at all, and among those who did, traders were net buyers of equities by nearly four to one. Most did not trade; the minority who acted mostly leaned the opposite way from the panic narrative. It is a useful mirror: the crowd you picture rushing for the exits is often smaller and less unanimous than the fear in your chest suggests. StockCram is not affiliated with Vanguard or any brokerage or firm mentioned here.

What history does not show is a rule you can trade on. It does not promise a bounce or a timeline, and every one of these episodes looked genuinely uncertain while it was happening, exactly as today does. The record is perspective, not a crystal ball.

Key Takeaway: Some war shocks were quickly recovered and one (1973) took years; history offers perspective, not a rule you can trade on.

Approximate S&P 500 moves around four geopolitical shocks (Citi/Citigroup market-reaction tables; figures rounded and vary across publications). Historical data is context, not a forecast.

| Event | Days 30 | Days 90 | Initial Drop |

|---|---|---|---|

| Cuban Missile Crisis (1962) | +8% | +17% | -4% |

| Gulf War (1990–91) | ~flat | +12% | -4% |

| 9/11 attacks (2001) | +0.5% | +4% | -12% |

| Arab Oil Embargo (1973) | -8% | -13% | -16% |

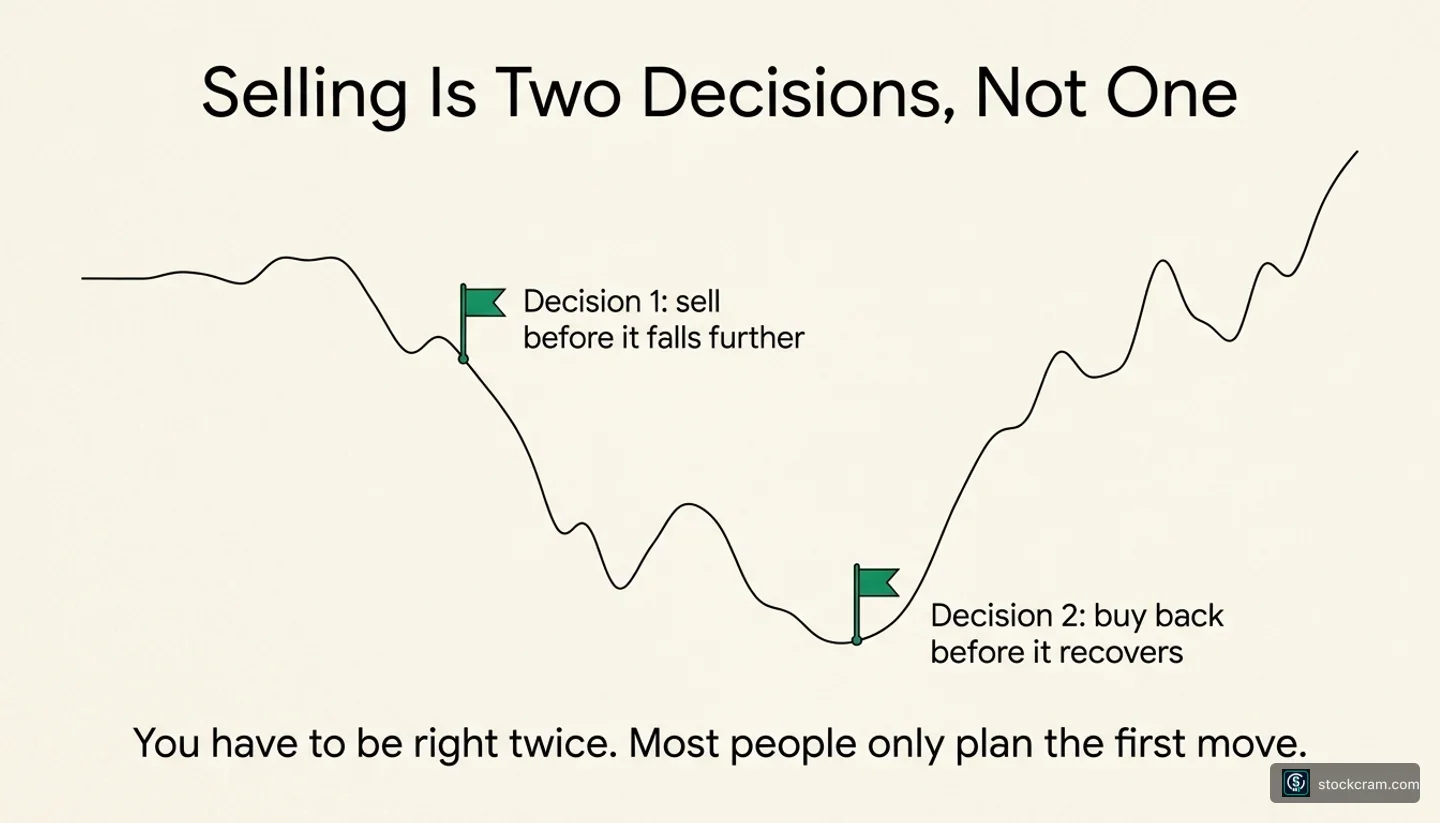

Selling feels like one decision. It is actually two, and the second is the hard one nobody mentions in the moment.

Decision one is when to get out. It feels urgent and obvious: the headline is scary, so exit. Decision two is when to get back in, and it determines whether the whole move helped or hurt. The day you sell, you have signed up for a second call: at what point do you return? Most people who panic-sell never plan this part, and that is where the trouble lives.

Getting the round trip right means being correct twice. You would need to get out ahead of a further decline and then back in ahead of the recovery, all while the news is still frightening and every instinct is screaming to stay in cash. This is market timing, one of the hardest things to do consistently in investing, because the re-entry point never arrives with a bell.

Pictured on a price chart, the trap is easy to see:

Recoveries after war shocks, when they have happened, have often been fast and front-loaded. Look at the table: some of the biggest moves came in the first weeks off the bottom, while the headlines were still ugly. If you are in cash waiting for the news to feel safe, it almost never feels safe at the exact moment the market turns. By the time the all-clear feeling arrives, a good chunk of the recovery has usually already happened, and you are deciding whether to buy back higher than you sold. That is how a fear-driven exit can lock in a loss a paper dip never would have.

None of this means selling is wrong for everyone. It means that if you are weighing it, you owe yourself a clear answer to the second question before acting on the first. What is your actual re-entry rule: a price, a date, a feeling? If the answer is 'I will just know,' look again, because 'I will just know' is often what recency bias and herd behavior sound like when they pretend to be a plan. The point is not to freeze. It is to look at both halves of the decision, not just the half fear is shouting about.

Key Takeaway: A sell is really two calls, and the second (when to buy back) is the one panic never plans; getting the round trip right means being correct twice.

To tell a reaction apart from a decision, questions work better than rules. None of these decide it for you. Each is a mirror for checking whether today's headline touched your plan or only your pulse. Sit with them before you touch anything.

Has my time horizon changed? Time horizon is how long until you actually need this money. A headline does not move that date. If you did not need these dollars for fifteen years yesterday, a war scare has not changed the number of years, even if it changed how the wait feels. If your horizon genuinely shifted for reasons unrelated to the news, that is a real planning input.

Do I have a near-term cash need I forgot to fund? If a tuition bill, a down payment, or an emergency lands in the next year or two, money you truly need soon arguably should not have been exposed to daily volatility in the first place, war or no war. Noticing that now is useful. The trigger, though, is your calendar, not the headline.

Did anything about why I own this actually change? Ask whether the war altered the specific reason you bought what you own, or only the mood around it. A correction or even a bear market driven by a fear premium is different from a permanent change in what you own. Sometimes something real changed. Often the reason you own it is intact, and only the price and the mood moved.

Am I too concentrated to sleep? If a single stock, sector, or bet is large enough that this week is genuinely threatening your finances or your rest, that is information about how the portfolio was built, not about the war. Concentration is what turns a market wobble into a personal crisis. That is a structural question worth examining calmly, ideally not mid-session.

Is my risk level honestly matched to me? A war scare is a brutally effective stress test. If this drawdown feels unbearable, it may be revealing that the risk you carried was higher than the risk you can live with. That is worth learning. The trap is letting the scariest possible moment set your permanent risk level, because fear overshoots in exactly one direction.

Notice the shape of every question. Each asks whether something in your situation changed, not whether the headline is frightening. War headlines are frightening; that does not mean every frightening headline changes your finances. Underneath all five sits one question: did anything practical change? Answer that honestly and you have done the hardest and most valuable part, whichever way you decide.

Key Takeaway: Planning questions all reduce to one: did anything practical change, or is the headline just frightening? That distinction, not a rule, separates panic from a plan.

A whole body of long-term investing thinking exists precisely because headlines like today's are unpredictable. The useful thing is not to follow any of it as an order but to see what problem each idea was built to solve. We are describing them, not prescribing them.

Buy-and-hold stays invested through cycles instead of jumping in and out around events. Buy-and-hold does not claim nothing bad will happen; it bets that reacting to each scare costs more than it saves, for the two-decision reason above. Its design assumption is that frightening headlines keep coming and most will not have mattered in hindsight.

Diversification stops your outcome from depending on any one company, sector, or event, so no single headline, war included, can be decisive. That is the whole point: single-event outcomes are unpredictable, so you arrange things not to need the prediction.

Rebalancing nudges a portfolio back toward its target proportions after prices push it out of shape. Notice what it answers to: a predetermined target on a schedule, not how frightening the news feels today.

Dollar-cost averaging invests a fixed amount on a regular schedule regardless of the market. Dollar-cost averaging takes the timing call, the one fear corrupts most, off the table by letting the schedule decide. Some people also cite mean reversion, the historical tendency of markets to swing back toward long-run averages, though that is an observation about the past, not a guarantee.

The thread is simple: each idea removes a decision emotion is bad at making. They automate away the exact moment you are living through. Whether any fits you depends on your goals and circumstances, which is a question for you and, if you want one, a licensed professional who knows your situation.

Key Takeaway: Long-term frameworks share one design goal: automating away the panic-prone decision you are facing right now. They are concepts to understand, not orders to follow.

If you take nothing else from this piece, take a pause. When a war headline has your finger over the sell button, the most useful move is to insert a short, boring gap between the feeling and the action. The checklist below is built for that gap. It does not tell you to sell or to hold; it just helps make sure that whatever you decide is a decision and not a reflex.

Try this one-sentence self-check first. Finish the sentence: 'I am selling because ______.' If the blank is 'I feel scared,' that is a signal to pause. If it is 'I need this cash within a year,' that is a real planning reason. If it is 'everyone says it gets worse,' pause again and check the facts. It is a mirror, not an instruction.

Notice what the checklist questions share: almost every one points back at your own situation and away from the headline. A trade that still makes sense after you have honestly worked through them is a planned trade, whatever it turns out to be. A trade that only made sense while your heart was racing is the one these prompts are meant to catch. The headline will still be there in an hour, and the button will still be there tomorrow.

If you are still unsure after all that, that is a reasonable place to be, and a good moment to talk to a licensed financial professional who can look at your actual circumstances rather than a generic page. Uncertainty is not a signal to act fast. It is usually a signal to slow down.

One thing before you close the tab: save this checklist before the next scary headline.

Key Takeaway: Before any war-headline trade, insert a boring pause and run the checklist; a decision that still holds afterward is a plan, and one that doesn't was a reflex.

You cannot control the war. You cannot control whether the Strait of Hormuz stays open, what any government does next, or where the market closes on Friday. Spending energy predicting those things spends it on the one part entirely outside your hands.

What you can control sits closer: your reaction. Whether you let a headline convert a temporary feeling into a permanent decision is up to you, and it is where nearly all the avoidable damage in these moments happens. The market did what it did in the table above regardless of how anyone felt; the difference between investors was in what they did next.

So the frame we leave you with is the one we opened with. When the next frightening headline lands, and there will always be a next one, the useful question is not 'will it get worse.' Nobody knows. The useful question is: did this change my plan, or only my feelings? If your plan genuinely changed, adjust it deliberately, ideally with a professional who knows your situation. If only your feelings changed, you have met volatility behaving the way it routinely does, and the calmest move is often to let the feeling pass before deciding anything.

None of this is a recommendation to buy, sell, or hold, and none of it is a forecast. This lesson does not expire when the current headlines fade, which is the point. Wars, elections, crashes, and crises will keep arriving. The reaction is the part you own every time, and learning to read your own reaction is the most durable investing skill there is.

Want a calmer way to follow market headlines? Create a free StockCram account to save guides like this to your dashboard.

Key Takeaway: The war is outside your control; your reaction is not. The controllable risk in front of you is turning a temporary feeling into a permanent decision.

Short answers to the questions people ask most when a war headline has their portfolio in the red.

This piece is the behavioral corner of a larger set. If you want the mechanics behind the headlines rather than the psychology of reacting to them, these companions go deeper, each in its own lane:

All four are part of our Market Explainers series. And for a parallel example of the same behavioral pull in a very different setting, are we in another AI bubble? looks at how the crowd's mood shapes reactions to hype rather than to fear.

Key Takeaway: Use the companion guides for the mechanics of war and markets; this piece stays focused on how to read your own reaction.

This guide draws on reported news and published research, credited here as a transparency and credibility signal.

Key Takeaway: Reporting from AP and Reuters, historical data from Citi/Citigroup, behavior data from Vanguard, and education from FINRA and SEC Investor.gov.

This is a planning question, not a yes-or-no

Whether to sell depends on your timeline, your portfolio, and whether your situation changed, none of which a headline decides. The reframe: did anything practical change, or did my body just react?

The urge to sell is a fear loop, not information

Loss aversion, recency bias, and herd behavior push toward the sell button; none of the three is a fact about when you actually need your money.

History gives perspective, not a rule

Markets recovered within months after some war shocks (1962, 1990–91, 2001) but took years after 1973; the future stays uncertain.

Selling is two decisions, and the second is the hard one

You have to be right about when to get out and when to get back in, while recoveries often start before the news feels safe.

The reaction is the part you can control

You cannot control the war or the market, only whether you turn a temporary feeling into a permanent decision. That skill never expires.

Is the housing market crashing in 2026? The truer answer: it's frozen, not crashing. The lock-in effect, both sides, in plain English.

You've heard "high rates are bad for stocks," yet stocks are near record highs. Here's the plain-English why, both sides, anchored to the 2026 market.

At Kevin Warsh's first meeting, the Fed held rates in June 2026, but flipped its signal toward a hike. A plain-English decode of what happened and why it matters.

No one can answer that for you; a flat yes or no would be guessing about your life. Whether selling fits depends on when you need the money, how your portfolio is built, and whether anything in your situation actually changed, none of which a headline touches. The more useful question is whether the war changed your plan or only how you feel. If your plan genuinely changed, adjust it deliberately, ideally with a licensed professional. If only your feelings changed, that is volatility behaving normally. This is education, not advice.

Often there is an initial drop, but what happens to stocks during a war has varied a lot. Around the Cuban Missile Crisis (1962), the Gulf War (1990–91), and 9/11 (2001), the S&P 500 fell at first yet was higher ninety days later. The 1973 Arab Oil Embargo is the counterexample: stocks fell about 16%, were still down about 13% three months on, and the surrounding bear market took years to recover. Shocks that genuinely hurt the real economy behaved very differently from shocks that were mostly fear. Figures are approximate (Citi/Citigroup); past performance does not indicate future results.

Because your brain is running a fear loop, not a spreadsheet. Loss aversion makes a drop hurt more than an equal gain feels good, recency bias makes today's decline feel like the start of a trend, and herd behavior makes selling feel safe when everyone else is doing it. Together they produce the urge that defines panic selling. Recognizing the loop buys you a moment to check whether anything in your plan actually changed.

It depends on what you mean by safe and over what period. Cash does not swing day to day, so it feels safer during a scare, and money you need in the next year or two is a different question from long-term money. Over longer stretches, cash carries its own risk: inflation erodes its purchasing power, and stepping out means facing the re-entry problem of deciding when to return. There is no universally safe choice, only trade-offs that depend on your timeline.

A 401(k) is not a single investment; it is an account holding the funds you chose inside it, often stock funds, bond funds, and target-date funds. Moving it 'to cash' usually means switching those funds into a money-market or stable-value option, which locks in whatever the balance is that day and hands you the re-entry problem: deciding when to switch back, while the news still feels bad. For most people a 401(k) is long-term, retirement-horizon money, a different time horizon from cash you need soon. How it is structured we can explain; the right mix depends on your circumstances and is a good topic for a licensed professional. This is not allocation advice.

There is no universal answer, and anyone who gives you one is guessing. Which path fits depends on your timeline, your cash needs, how your portfolio is currently built, and whether the reason you own your investments changed, not on the headline itself. The stock market during war has reacted in very different ways to different shocks, so the past offers perspective rather than a rule. Investing during a geopolitical crisis feels different, but the decision structure is the same: the useful step is telling whether today's news changed your plan or only your mood. This is educational, not a recommendation.

There is no fixed answer. In some past cases recovery came within weeks or months (the market was higher ninety days after the 1962, 1990–91, and 2001 shocks). In others, like the 1973 oil embargo, it took years. When rebounds did come, much of the move often arrived early, which is exactly why timing your exit and re-entry is so hard: the recovery tends to start while the news still feels bad. Figures are approximate; the future stays uncertain.

Panic selling is selling in a rush, driven by fear and crowd pressure rather than by any change in your plan or the reason you owned the investment. It sits at the end of the fear loop: loss aversion and recency bias make a drop feel unbearable, herd behavior makes selling feel safe, and the sell button promises instant relief. The tell is the motivation. A sale prompted by a real change in your situation is planning; a sale prompted mainly by how a headline felt is panic selling.