Robinhood Agentic Trading: How It Works and the Risks

Robinhood agentic trading lets an AI agent place trades in a dedicated, funded account. A calm, plain-English walkthrough of how it works and the risks.

15 min read

Read Article

Three AI giants approached public markets in 2026 at a combined ~$3.6T target, but the paths diverged. SpaceX went public June 12 with a record IPO, then slid below its $135 offer price; Anthropic is on track for an October 2026 listing under ANTH; OpenAI has delayed, now eyeing 2027.

Educational purposes only. This content does not constitute investment advice. Read our disclaimer

StockCram is not a broker-dealer, investment adviser, or financial institution. All content is for educational and informational purposes only and should not be construed as personalized investment advice. Consult a qualified financial professional before making investment decisions. Past performance does not guarantee future results.

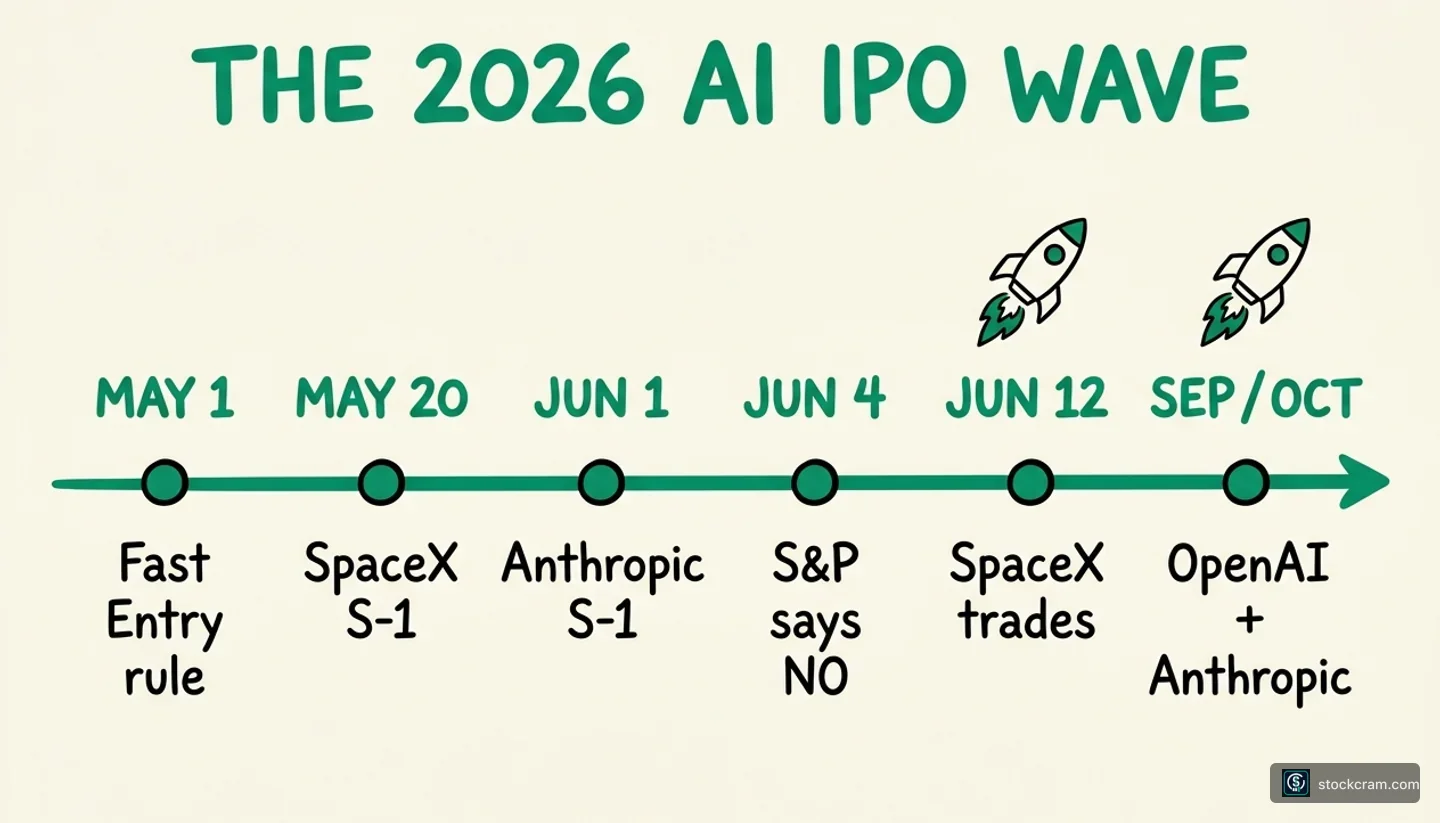

In a single 14-day window starting June 12, 2026, the U.S. stock market will absorb the largest IPO in history. Eight days later, the dust will still be settling on SpaceX (now combined with xAI) when Anthropic's confidentially-filed S-1 picks up its road toward an October listing. OpenAI's filing (even quieter, but already in) sits behind them. Three companies, roughly $3.6 trillion of combined target valuation, and the SEC's IPO machine all moving at once.

The 60-second version of the AI IPO wave debate: Bears say this is the textbook bubble-top signal: mega-IPOs at all-time highs concentrated in one sector that already makes up ~35% of the S&P 500. Bulls say these are *profitable, revenue-real companies* (not 1999 pets.com), and a new NASDAQ-100 rule will force passive index funds to buy whether they want to or not. Both sides have real numbers. Here's the long version.

We'll walk through each of the three IPOs (what the company is, what it's worth, when it lists), surface the *one* angle nobody else is explaining clearly for beginners (forced index buying), compare this wave to past mega-IPOs, and lay out what each side is actually arguing. This is Article 2 of our Market Explainers series and the launch piece for a new sub-series specifically on the trillion-dollar IPO wave. For the broader AI bubble debate, see Article 1. One note before we start: the figures and dates in this article are based on publicly available reporting as of June 7, 2026. Several key numbers (final IPO valuations, allocations, prospectus details) may change before the official documents are released. Where a figure is media inference rather than a primary-source disclosure, we'll call it out specifically. Update, June 8, 2026: Three developments since publication. (1) SpaceX's institutional order book is reportedly ~2× oversubscribed, roughly $150B of demand for the $75B raise (Bloomberg, June 8). Institutional orders close June 10. (2) OpenAI publicly confirmed its confidential S-1 filing via a company blog post today, upgrading the May 22 filing from media-reported to company-acknowledged. (3) Analysts now estimate ~$50B of selling pressure on *other* stocks as institutions reposition portfolios to fund SPCX purchases, the wave is starting to move cross-market money before SpaceX even trades. We'll cover SpaceX's specific trading dynamics, lockup mechanics, and VC payday math in the dedicated SpaceX deep-dive after the June 12 listing. Update, June 11, 2026 (pricing day): SpaceX officially priced this evening at $135/share on 555,555,555 shares for a $75 billion raise (NPR; CNBC). Underwriters also hold an option for an additional 83.3M shares (greenshoe). The 30% retail allocation (~$22.5B) is the largest direct-to-retail carve-out any mega-IPO has ever extended. The S-1 also revealed a staggered, non-standard insider lockup, not the usual 180-day cliff but tiered releases tied to Q2 and Q3 earnings; Musk is locked up for one full year (CNBC, May 21). First trade is tomorrow, June 12, see our SpaceX deep-dive for the full lockup schedule, retail-fill math, Day-1 LULD-halt mechanics, and the Morningstar bear case. Update, June 16, 2026: The wave's first member is now public. SpaceX began trading June 12 as `SPCX` and, after closing its first day at $160.95 (+19% over the $135 IPO price), ran to around $200 by June 16, carrying its market value above $2 trillion. The other two are filed and preparing to follow: Anthropic submitted a confidential S-1 on June 1 (reportedly around a $965 billion valuation, with a listing eyed for roughly October), and OpenAI followed on June 8 (a September debut at $1 trillion-plus is the reported target). Together the three represent roughly $3.6 trillion of listings. Our SpaceX deep-dive covers the actual debut in detail. *Historical data shown; past performance does not indicate future results.* (Investing.com; CNBC; TheStreet.) Update, July 26, 2026: The wave has diverged from the picture above, and is now mixed rather than uniform. SpaceX gave back its gains: after reaching $225.64 on June 16 it fell below its $135 IPO price by mid-July, trading around $113 on July 25 (an all-time low of $110.85 on July 23). Anthropic remains on track for an October 2026 Nasdaq listing under the ticker `ANTH`, with investor meetings held in mid-July, and could be the first company to go public near a $1 trillion valuation. OpenAI has delayed: reporting now points to a 2027 listing rather than 2026 (Bloomberg, June 26). The sections below were largely written before the June 12 listing; read the dated updates above as historical snapshots. *Historical data shown; past performance does not indicate future results.*

Update, reviewed July 26, 2026: The wave has diverged, and it is now mixed rather than uniform. SpaceX went public June 12 as SPCX at its $135 IPO price, popped to $160.95 on Day 1 (+19%) and reached $225.64 on June 16, then fell back below its $135 IPO price by mid-July; it traded around $113 on July 25 (an all-time low of $110.85 on July 23), a rocky post-IPO debut. Anthropic remains on track, targeting an October 2026 Nasdaq listing under the ticker ANTH, and could be the first company to go public near a $1 trillion valuation (underwriters Goldman Sachs, JPMorgan, and Morgan Stanley; investor meetings were held in mid-July). OpenAI has delayed: after a June 8 confidential filing, reporting (Bloomberg, June 26) now points to a 2027 listing rather than 2026, citing market volatility, SpaceX's rocky debut, and CEO Sam Altman's insistence on a roughly $1 trillion listing floor. One member is public and below its offer price, one is proceeding, one has slipped to 2027. Historical data shown; past performance does not indicate future results.

The wave at a glance: read this and skip ahead if you're short on time, or keep going for named voices, dated sources, and the killer angle.

The three companies in one sentence each. SpaceX (combined with xAI since February 2026) trades June 12 on NASDAQ as SPCX at a ~$1.75 trillion target, with up to a $75 billion raise, 2.5× larger than Saudi Aramco's record. Anthropic filed a confidential S-1 on June 1 with a ~$47 billion annualized run-rate (a 12-month projection of the most recent month's revenue, not actual booked annual revenue); Bloomberg reports an October listing target on NASDAQ. OpenAI is reported to have filed confidentially on May 22; recent reporting (Reuters and The New York Times, late June 2026) now points to a possible 2027 listing rather than a 2026 debut, and Sam Altman has publicly said timing is undecided.

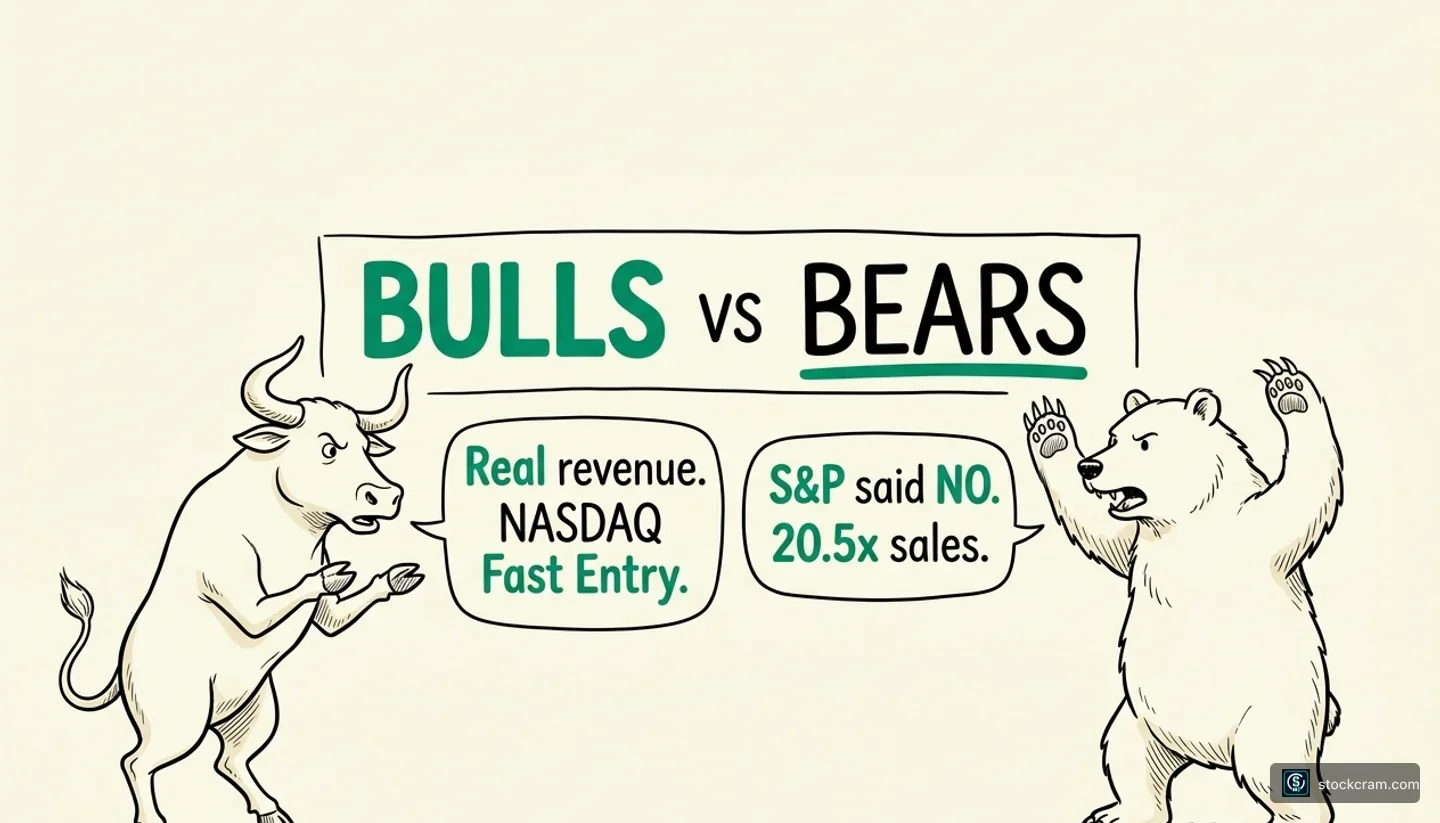

The bull case, in summary, is that these are real-revenue, audited, mostly-profitable companies, a structural break from 1999's pets.com IPOs, and that a new NASDAQ-100 "Fast Entry" rule (effective May 1, 2026) auto-includes top-40-by-market-cap names after just 15 trading days, creating mechanical NASDAQ-100 demand within weeks of each IPO. (S&P Dow Jones declined to follow on June 4, keeping the S&P 500's existing profitability and 12-month-seasoning rules in place.) Anthropic President Daniela Amodei, Wedbush's Dan Ives, and PIMCO and BlackRock's published commentary all sit on this side.

The bear case is that mega-IPOs at all-time highs concentrated in one sector are textbook late-cycle, and that Anthropic at $965 billion against a $47 billion run-rate is ~20.5× sales, the upper end of comparable enterprise software. Michael Burry on his Substack, Jeremy Grantham of GMO in Fortune, and, uncomfortably, Anthropic CEO Dario Amodei's own "if I'm off by a year… you go bankrupt" line from Dwarkesh Patel's podcast all sit on this side.

Both camps agree on the facts: the index-inclusion mechanics will apply mechanical buying, and the wave's scale is unprecedented. What separates them is whether the mechanical bid is foundational (proves AI's economic weight) or artificial (passive flows masking fundamentals that haven't caught up yet). The disagreement isn't about the data. It's about the future, which neither side can prove.

Key Takeaway: Three trillion-dollar AI IPOs in four months is without precedent in U.S. capital markets. Smart investors disagree about whether that's a feature or a warning.

Quick framing before we go deeper. This is a fast-moving story with three different kinds of facts mixed together: public S-1 filings (high confidence), confidential filings reported by reliable journalists but not yet public (medium confidence), and rumors / leaks / inferences (lower confidence). Treating them as equivalent is how readers get burned. The table below separates them.

We'll cite each item with its strongest available source as we go through the article. When a figure is media inference (like Anthropic's widely-cited "$965B IPO valuation," which is actually the Series H post-money number rather than an S-1 target), we'll call it out specifically.

Key Takeaway: Three categories of facts in one story. Trust the public S-1 filings most, treat reported items as reasonable inference, treat rumors as scenarios, not certainties.

All three IPOs are at different stages of disclosure. As of June 5, 2026.

| Items | Status |

|---|---|

| SpaceX S-1 filed publicly May 20, 2026 · NASDAQ-100 "Fast Entry" rule effective May 1, 2026 · S&P Dow Jones declined to relax S&P 500 entry rules (June 4, 2026 announcement) · FTSE Russell adopted fast-entry rules for its global indices · Anthropic Series H closed May 27-28 at $965B post-money · Dario Amodei's Feb 2026 Dwarkesh Patel quote on tail risk | Confirmed (public filings + official sources) |

| Anthropic confidential S-1 filed June 1 (Fortune, CNBC) · OpenAI confidential S-1 filed June 8 · Goldman, JPMorgan + Morgan Stanley as Anthropic underwriters (Bloomberg June 3) · 30% SpaceX retail allocation · Anthropic $47B run-rate (Simon Willison, CNBC) · Anthropic October listing target under ANTH (Bloomberg) | Reported (credible journalism, not in primary documents) |

| Anthropic IPO valuation target ("$965B" is media inference from Series H, not an S-1 figure) · Tesla-SpaceX merger (Dan Ives 80% odds; Fortune June 4 spotted hint in amended S-1) · OpenAI listing timing (reporting now points to a 2027 listing rather than 2026; Bloomberg, June 26) · Final IPO allocations across institutional vs retail | Rumored / inferred (single source or speculative) |

Here's the calendar of what's known. Confirmed items in bold; reported timing in regular text.

The wave compresses roughly four months of unprecedented IPO activity into a single visual:

Five major milestones between May 1 and June 12, and the wave isn't even half-done: OpenAI and Anthropic are still ahead. The table below adds the granular detail.

Key Takeaway: The largest IPO in history (SpaceX) opened the window in June but has since traded below its offer price; Anthropic (the fastest-growing) is on track for an October listing under ANTH; OpenAI (the most strategically loaded) has slipped, with reporting now pointing to a 2027 listing.

Dates as currently known. Confidential filings stay private until ~21 days before the roadshow; expected listing dates are based on Bloomberg / CNBC reporting.

| Company | Roadshow | Filing Status | Expected Listing |

|---|---|---|---|

| SpaceX | June 8–11, 2026 | Public S-1 (May 20, 2026) | June 12, 2026 (NASDAQ: SPCX) |

| OpenAI | Delayed (reportedly now targeting 2027) | Confidential S-1 (June 8, 2026) | Delayed; reporting now points to a 2027 listing rather than 2026 (Bloomberg, June 26) |

| Anthropic | Reportedly September 2026 | Confidential S-1 (June 1, 2026, reported) | On track for October 2026 (NASDAQ: ANTH) |

Three confidential S-1 filings inside ten days isn't coincidence. It's structural.

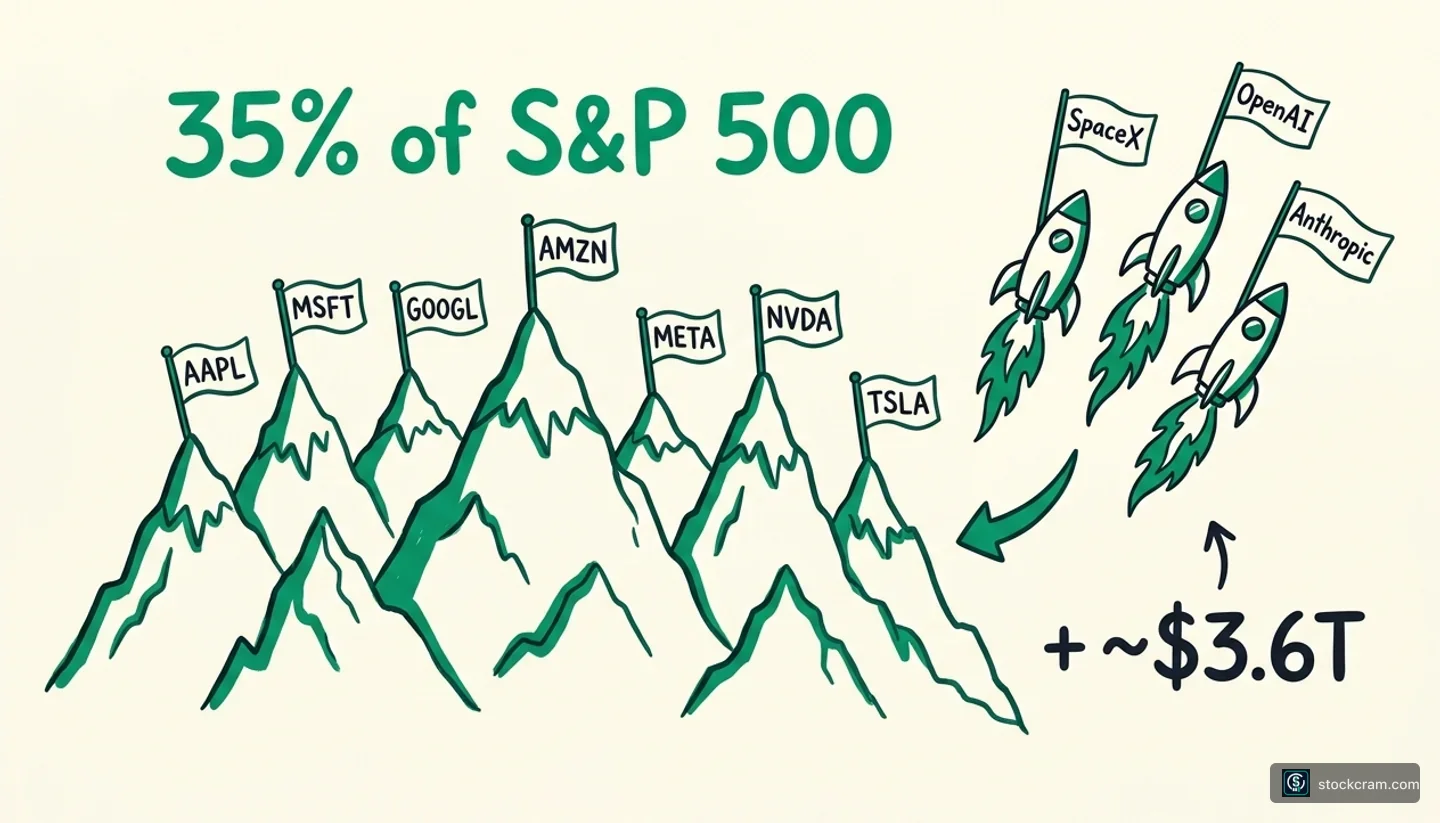

The market backdrop is hot. The S&P 500 is trading near 7,609 (June 3, 2026); the Magnificent 7 (Apple, Microsoft, Alphabet, Amazon, Meta, Nvidia, Tesla) collectively account for roughly 35% of the entire index by market capitalization; and hyperscaler capex is on pace for $700–725 billion in 2026 (covered in detail in Article 1). The chart below makes the concentration easier to feel than to read. If a company has any plausible reason to list public soon, this is the window.

More importantly, the rules of going public partly changed in spring 2026 in ways that favor these specific IPOs. The NASDAQ-100 "Fast Entry" rule (effective May 1, 2026) cut the seasoning requirement to just 15 trading days for new listings in the top 40 by market cap, and FTSE Russell has adopted parallel fast-entry rules for its US and global indices. S&P Dow Jones, however, went the other way: after a public consultation, on June 4, 2026 it confirmed it would not relax the S&P 500's existing 12-month seasoning, profitability, and float requirements, a meaningful setback for SpaceX, which now can't be considered for S&P 500 inclusion until at least mid-2027 and only if it becomes GAAP-profitable by then. We'll work through the math in Section 7, but the short version is that the NASDAQ-100 mechanic is real and immediate, the S&P 500 mechanic is not, and the gap between those two outcomes is one of the more important data points for reading the wave.

Layered on top is a forward-looking conversation worth bookmarking but not building a thesis around: Wedbush's Dan Ives now puts Tesla-SpaceX combination odds at 80-90% with a first-half-2027 target. Rumor-quality with credible analyst attribution, see our SpaceX deep-dive for the merger mechanics if you want them.

Add three trillion-dollar AI listings to the existing concentration picture and the implication becomes visual:

The Mag-7 already account for ~35% of the S&P 500. Adding the AI IPO wave doesn't diversify the index; it deepens the same bet on the same theme.

Key Takeaway: The wave isn't accidental. Companies, indices, and macro conditions all aligned at the same moment; that's structural, not coincidental.

Start with the company that went public on June 12. SpaceX filed its S-1 publicly, not confidentially, on May 20, 2026 (SEC EDGAR), and the roadshow launched June 4 (earlier than the originally reported June 8 window after a faster-than-expected SEC review). It priced after market close on June 11 and began trading June 12 on NASDAQ as SPCX at a ~$1.75 trillion valuation. Unusually, SpaceX bypassed the traditional price-range process and went straight to a fixed $135 per share on 556.6 million shares, which signals confidence in book demand. The raise, up to $75 billion, would be 2.5× larger than Saudi Aramco's 2019 record (which raised $25.6B, or $29.4B counting the greenshoe).

The profitability question matters because S&P 500 entry depends on it. SpaceX's S-1 disclosed 2025 revenue of $18.67 billion (+33% YoY) and a net loss of $4.94 billion, which is why S&P Dow Jones declined on June 4 to relax the index's profitability requirement, blocking SpaceX from S&P 500 fast entry. NASDAQ-100 Fast Entry remains in play; S&P 500 inclusion is now off the table until at least mid-2027.

The company going public is no longer the SpaceX of two years ago. SpaceX absorbed xAI in February 2026 in an all-stock transaction at a combined ~$1.25 trillion valuation ($1.0T SpaceX + $250B xAI), so what trades on June 12 is a launch + Starlink + AI infrastructure conglomerate. That breadth cuts both ways: bulls point to diversified revenue across launch contracts, Starlink subscriptions, and AI compute; bears note that no comparable trading multiple exists for an integrated company like this.

The underwriting syndicate is first-tier, Goldman Sachs lead with Morgan Stanley and JPMorgan in the book (CNBC, May 20, 2026; PYMNTS, June 3, 2026). Not a regional or boutique-led offering.

What's notable is the retail allocation: SpaceX is reportedly setting aside up to 30% of the offering for retail investors via Robinhood's IPO Access, Fidelity, and Charles Schwab. (StockCram is not affiliated with any brokerage mentioned.) Mega-IPO retail allocation is typically under 10%, so 30% is a structural break, one that may translate into heavier retail demand at the open and more first-day volatility in either direction.

The Tesla-merger story is the section's wild card. Fortune (June 4, 2026) flagged a single sentence in SpaceX's amended S-1 that may signal the long-rumored Tesla-SpaceX combination, and Wedbush's Dan Ives publicly put the odds at 80%. The merged entity would be valued at roughly $3.4 trillion and would reportedly trigger Musk's $1 trillion Tesla compensation package automatically (per Electrek). There has been no on-the-record Musk statement either way. Treat the merger as material rumor, not confirmation.

The questions first-day watchers cared about were tactical: did the $1.75T target hold at pricing, was there a pop or a discount, and how institutional-versus-retail-heavy was the actual allocation book. In the event, SpaceX priced at $135, closed Day 1 at $160.95 (+19%) and reached $225.64 on June 16, then fell back below its $135 IPO price by mid-July, trading around $113 on July 25 (an all-time low of $110.85 on July 23). The rocky debut is a data point on whether the wave has the institutional backstop bulls expected. Historical data shown; past performance does not indicate future results.

Key Takeaway: SpaceX is the wave's lead story, biggest, most retail-accessible, and earliest. After an early pop it has since traded below its $135 IPO price, a rocky debut. The Tesla angle is the wild card.

This question comes up enough in our inbox that it deserves its own section. The short version: probably yes, but the path is narrower than the headline 30% retail-allocation number suggests.

SpaceX's roadshow reportedly routes retail allocation through Robinhood IPO Access, Fidelity, and Charles Schwab. (StockCram is not affiliated with any brokerage mentioned.) Each channel sets its own eligibility (minimum account balances, account history, sometimes invitation-only access) and none of them guarantees a fill. "Retail allocation available" is not the same thing as "every retail account that requests 100 shares will get 100 shares."

The 30% figure itself is worth a careful read. The headline is that SpaceX is setting aside up to 30% of the offering for retail, much higher than the typical <10% on a mega-IPO. But "the offering" is the shares sold at the IPO price, not the float that trades on Day 1, and the 30% is spread across all eligible retail investors using the participating brokerages combined. Demand will likely exceed allocation, in which case fills are partial or zero.

Three realistic paths exist for most readers, and they aren't equally available. The first is requesting shares at the IPO price through Robinhood, Fidelity, or Schwab IPO Access, eligibility varies and submission doesn't guarantee a fill. The second is buying on the open market on June 12, once SpaceX trades on NASDAQ as SPCX; anyone with a brokerage account can buy at the market price, which may be materially above or below the IPO price. The third, and arguably the simplest, is gaining exposure via index ETFs after inclusion: once SpaceX enters the NASDAQ-100 (~15 trading days after listing under Fast Entry), any NASDAQ-100 ETF such as QQQ gets weighted SpaceX exposure automatically. That's the passive bid we covered earlier, working in your favor instead of against you.

One caution on the open-market path. First-day mega-IPO prices are unusually volatile. Aramco opened flat-to-down. Meta closed near its IPO price on Day 1 but cratered weeks later. Alibaba popped 38% on Day 1. There is no reliable pattern for which way Day 1 breaks, even when the IPO is broadly considered hot.

None of the three paths is a recommendation. The map exists so readers can plan rather than panic-decide on listing day; whether SpaceX (or any of the three IPOs) belongs in a specific portfolio depends on the portfolio, not on whether the headline is exciting.

Key Takeaway: Retail access exists but isn't guaranteed. The simplest exposure for most readers, if they want any, is via NASDAQ-100 ETFs once SpaceX enters the index after Fast Entry.

Of the three filings, Anthropic's is the most extraordinary on the numbers, and the easiest to misread on the valuation.

Anthropic filed its confidential S-1 on June 1, 2026, targeting a NASDAQ listing under the ticker ANTH; as of late July it remains on track for an October 2026 listing (Bloomberg, June 3, 2026), with Goldman Sachs, JPMorgan, and Morgan Stanley leading the underwriting and investor meetings held in mid-July. If it prices near its private valuation, it could be the first company to go public near a $1 trillion valuation. That's the procedural baseline. What gets misread is the valuation everyone keeps quoting.

The widely-cited "$965 billion Anthropic IPO valuation" is not an S-1 target. It's the post-money valuation from Anthropic's Series H round, which closed May 27–28, 2026 on a $65 billion raise. The confidential S-1 itself doesn't set a target, that comes later, in the amended S-1 that becomes public ~21 days before the roadshow. So when headlines say "Anthropic going public at $965B," what's happening is media inference from the last private round, not a number Anthropic has filed with the SEC. The distinction matters because bears comparing $965B to revenue and bulls modeling forward IPO pricing may not be looking at the same number at all.

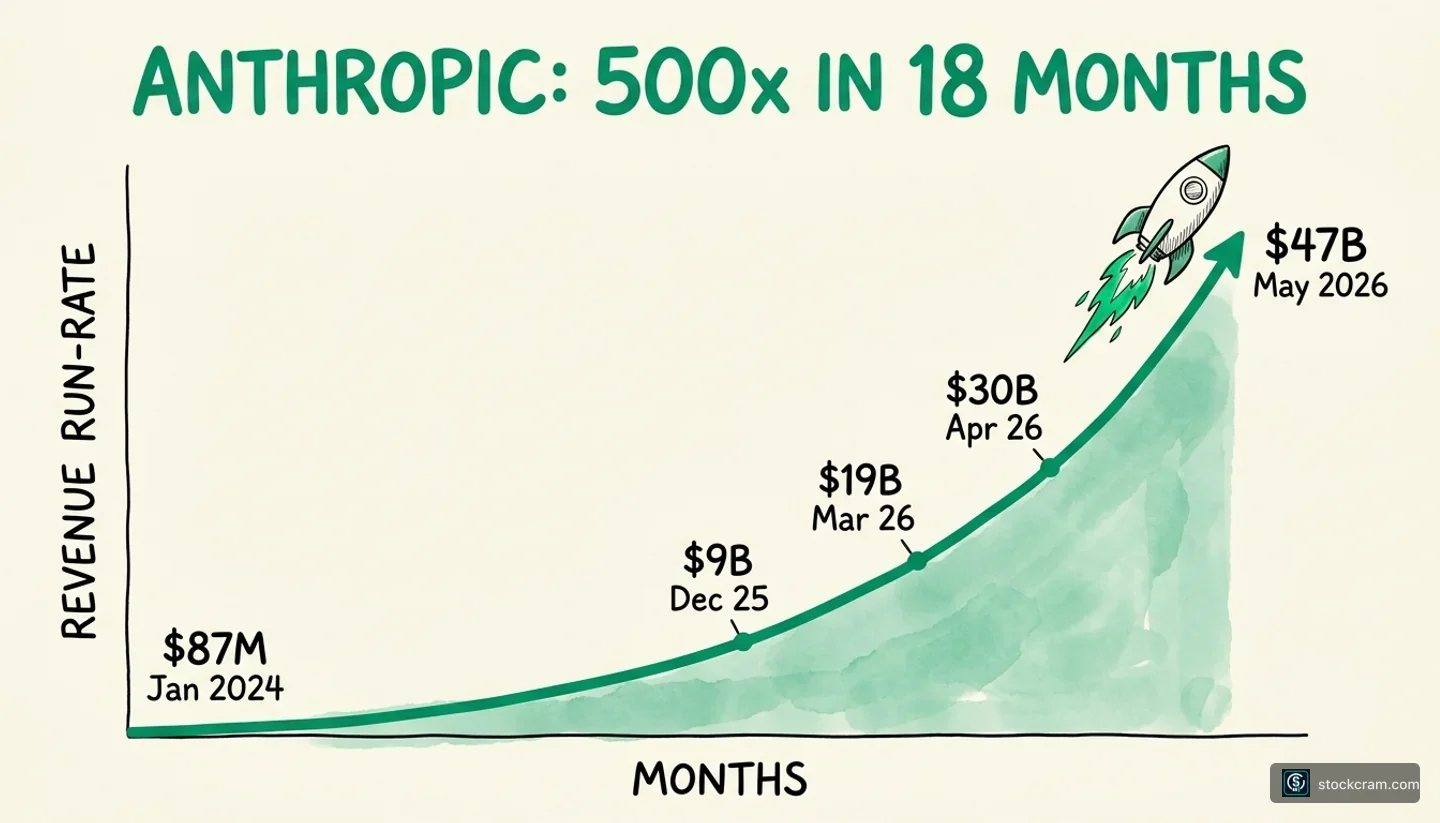

What is extraordinary is the revenue trajectory. Anthropic went from an $87 million run-rate in January 2024 to a $47 billion run-rate in May 2026, roughly 500× in eighteen months. Claude Code alone is reported at a $2.5 billion run-rate (Simon Willison, May 29, 2026; CNBC, May 28, 2026). That curve is the bull case condensed into a single chart, and the bear case is one observation about it: every published version of the chart has to compress the early months into a flat line near zero because the y-axis has to span from $87 million to $47 billion. The visual is genuinely hard to draw without distorting it, which is part of why pre-IPO valuation arguments around Anthropic keep talking past each other.

Drawn as the literal hockey-stick it is, the trajectory is hard to argue with, and equally hard to extrapolate:

The same data Anthropic execs see on their internal dashboard. Whether you're a bull or a bear, every argument about Anthropic's $965B valuation begins with this curve.

The share structure is unusual in a way investors should understand before buying Class A. Anthropic uses a multi-class stock structure: Class A (institutional, low vote), Class B (founders, higher vote), and Class T held by a Long-Term Benefit Trust with five independent trustees (Matheny, Bahl, Shah, Christiano, Robinson). The Trust gets an increasing share of board control over time, so the governance migrates away from any individual shareholder over the holding period, a more restrictive arrangement than Google's or Meta's dual-class setups.

The margin disclosure is unusually candid for a pre-IPO. The Information reported a recent Q2 operating profit of ~$559M on $10.9B revenue, and Anthropic itself flags that the figure is inflated by ramp-up discounts on its SpaceX compute deal and "won't last." Inference gross margin is reportedly improving from ~38% to 70%+ over the next two years. Set against that is the compute-concentration risk: Anthropic is committed to $1.25 billion per month with SpaceX Colossus 1 (Memphis) through May 2029, and AWS reportedly accounts for ~60% of total compute spending (per KeyBanc analysis). Two suppliers effectively control most of Anthropic's capacity.

On the multiple itself: at $965B against a $47B run-rate, Anthropic would IPO at approximately 20.5× revenue. For context, Nvidia trades around 25× sales, Snowflake around 12×, Microsoft around 13×. So Anthropic's multiple is at the upper end of comparable enterprise software, not absurd against its peers, but not cheap either. That valuation only makes sense if you believe the $47B run-rate is going somewhere much bigger, which is exactly the assumption every side of the debate is stress-testing.

Key Takeaway: Anthropic's revenue trajectory is extraordinary. Whether the company is worth $965 billion depends on whether you think the curve keeps bending up, or starts to bend down.

OpenAI's IPO is the most strategically loaded of the three, and the one we know least about.

Reports indicate OpenAI submitted a confidential S-1 on June 8, 2026, off a last private valuation of $852 billion (Series H, March 2026, $122 billion round). Since then OpenAI has delayed: recent reporting (Bloomberg, June 26, 2026) now points to a 2027 listing rather than a 2026 debut, citing market volatility, SpaceX's rocky public debut, and CEO Sam Altman's insistence on a roughly $1 trillion listing floor. Altman has publicly said the company is "not focused on timing." So the filing is company-confirmed, even though the draft S-1 itself is not yet on the public record. The amended S-1 (public roughly 21 days before the roadshow) is the moment when actual numbers, governance structure, and Microsoft's exact equity stake stop being inference and start being prospectus statements. Until then, almost every specific figure in OpenAI coverage is sourced to leaks or analyst estimates rather than filings.

The leaked internals tell a striking story. OpenAI is reportedly projecting a $14 billion 2026 operating loss and not expecting profitability until ~2030 (The Information). ChatGPT consumer revenue is estimated at ~$12 billion, the same figure that anchors the broader AI bubble revenue-gap debate (Article 1 walked through this in more detail).

The Microsoft governance complication is the part nobody else has had to disclose in an S-1 before. Microsoft's $13+ billion of OpenAI investment reportedly grants it ~49% economic interest in the for-profit subsidiary, and OpenAI's non-profit-controls-for-profit corporate structure has no clean precedent in a public-markets context. How the amended S-1 explains it will be among the most-read pages of any prospectus this year, both because it determines what shareholders are actually buying, and because it sets a template every future AI-lab IPO will be measured against.

In short: OpenAI carries the largest valuation in the wave, the lowest current profitability, the most complex governance, and the deepest entanglement with the broader bubble debate. If you wanted to design an IPO that was simultaneously the bull case (huge revenue, huge growth, brand-name AI leader) and the bear case (huge losses, governance complications, sentiment-driven), it would look very much like this one.

Key Takeaway: OpenAI is the wave's biggest and most opaque story. The eventual roadshow will be the moment the S-1 numbers become public, until then, almost everything is inference.

The piece almost no beginner-facing coverage is explaining clearly is this: passive index funds are going to mechanically buy a meaningful chunk of these companies whether their managers think the price is right or not, but how much and via which indices changed materially on June 4, 2026.

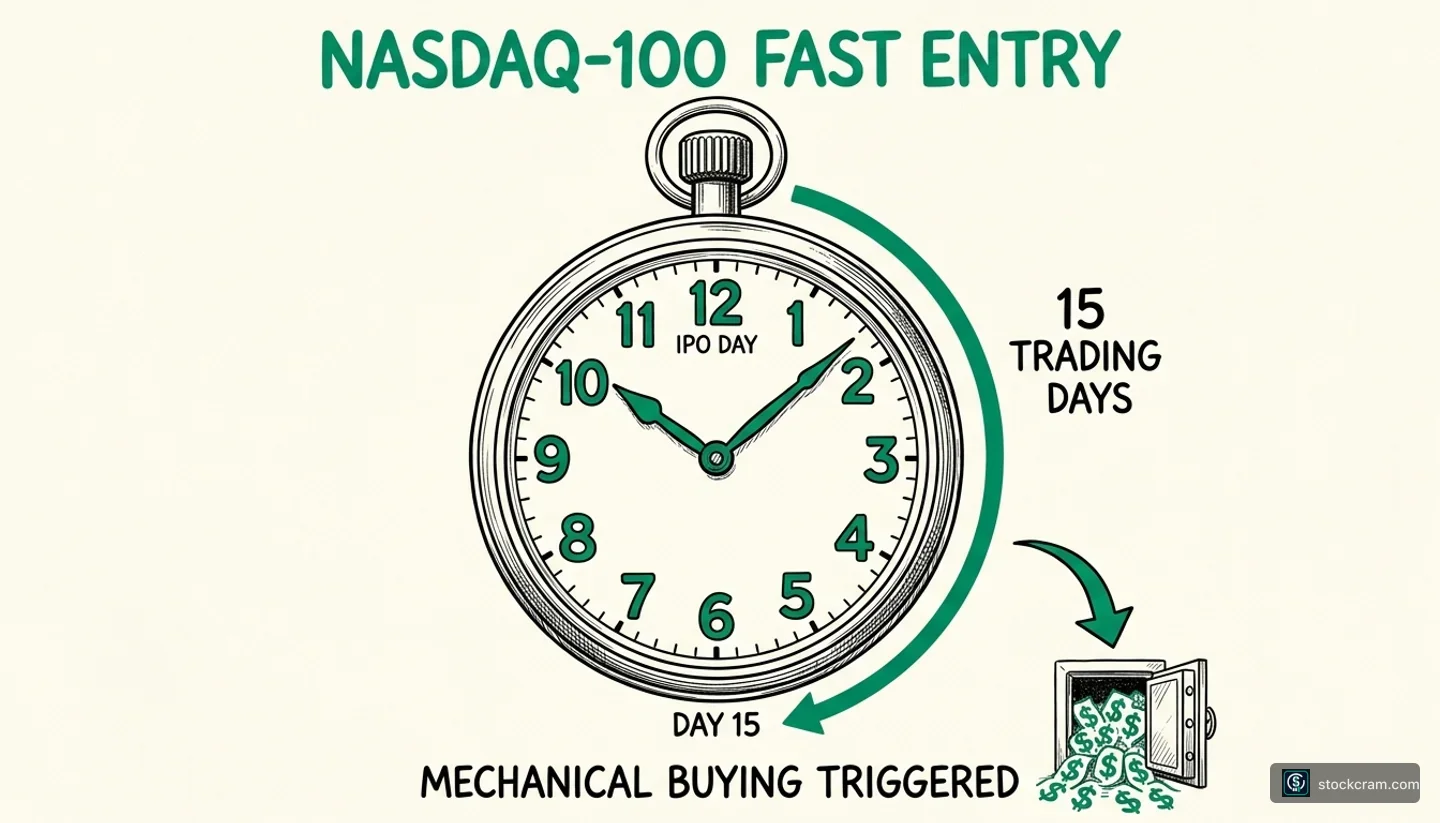

The NASDAQ-100 mechanic is the one that stands. On May 1, 2026, NASDAQ implemented a new "Fast Entry" rule for the NASDAQ-100 index methodology. Newly listed companies that rank in the top 40 by market cap can now enter the index after just 15 trading days of seasoning, with no prior liquidity requirements. Previously, names typically had to season for around six months. FTSE Russell followed in a parallel direction, adopting its own fast-entry rules; SpaceX is now already eligible for both the Russell US Equity Indexes and the FTSE Global Equity Index Series.

Visually, the NASDAQ-100 mechanic looks like a 15-trading-day countdown:

Once a top-40 IPO lists on NASDAQ, every passive NASDAQ-100 tracker is required to buy it within 15 trading days. The fund manager doesn't get to decide whether the price is right.

The S&P 500 mechanic is the one that didn't materialize. On June 4, 2026, three days before this article's publication, S&P Dow Jones announced after a public consultation that it would not relax the S&P 500's existing requirements (profitability, 12-month seasoning, and investible-weight-factor minimums). That's a hard no, not a delay. SpaceX, with $4.94 billion in 2025 net losses on the books, can't be considered for S&P 500 inclusion until at least mid-2027, and only if it becomes GAAP-profitable by then. Anthropic and OpenAI face the same gating. Bloomberg Intelligence estimates that S&P fast inclusion would have driven roughly $14 billion of forced passive buying into SpaceX alone. That's the bid that won't happen.

The NASDAQ-100 math, on its own, is still meaningful. QQQ alone tracks roughly $300 billion in AUM, and total NASDAQ-100 tracker funds add another several hundred billion on top of that. If SpaceX enters the NASDAQ-100 at a ~3% weight (reasonable for a $1.75T name), that translates to a low-double-digit-billions mechanical bid within 15 trading days of listing. Anthropic and OpenAI at ~1.5–2% weights each would draw less individually but compound the wave's total mechanical demand into the tens of billions. Smaller than the $4–7T combined figure that was floating around when S&P was thought to be in play, but still a structural tailwind that wouldn't exist without the rule change.

That buying is not optional. Index funds are required by their mandate to track their benchmark. If the benchmark adds a new constituent, the fund buys.

The bear reading came from Fortune (June 2, 2026): "If S&P Dow Jones rewrites its listing rules, SpaceX and Anthropic will benefit, investors won't." The bear argument was that forced inclusion would pump prices artificially: active managers wouldn't have bought at these valuations, but passive funds would have no choice. Two days after that piece ran, S&P Dow Jones effectively pre-empted the concern by holding the line. The bull reading is that NASDAQ and FTSE Russell's rule changes are correcting an outdated methodology, because modern strategic companies stay private longer (Anthropic was founded in 2021) and the old seasoning rules were systematically excluding the most important newcomers. S&P's stance is that the methodology shouldn't be rewritten for size alone, even when the size is unprecedented.

The cleanest historical comp is Tesla's December 2020 inclusion in the S&P 500. S&P Dow Jones' own indexology notes and contemporaneous Goldman Sachs / Morgan Stanley desk analyses put the required mechanical buying at roughly $51 billion, and the stock rallied about 70% in the six months that followed. Was that real demand, or index mechanics? The most-cited academic post-mortems land on "both, in roughly equal measure." Even the bears didn't dispute the mechanical bid happened. They disputed what it meant. The same disagreement is now hanging over the AI IPO wave, but with the S&P piece taken off the table the disagreement is more contained. The forced bid via NASDAQ-100 and FTSE Russell is real. Whether it's a tailwind, a partial bubble, or just a methodology fix is what the next 12 months will sort out.

Key Takeaway: Tens of billions in passive funds will be forced to buy these stocks via the NASDAQ-100 within weeks of their IPOs. The S&P 500 leg, which would have multiplied that figure several times over, is off the table after S&P held the line on existing rules.

Estimated mechanical buying from passive index funds upon NASDAQ-100 inclusion. NASDAQ-100 numbers are estimates based on target valuations, indicative weights, and a NASDAQ-100 tracker AUM base in the high hundreds of billions; actual figures depend on final market cap at inclusion. S&P 500 fast entry was denied by S&P Dow Jones on June 4, 2026, that column is the bid that won't happen until profitability gates are met. Bloomberg Intelligence's $14B SpaceX-specific S&P estimate is included for reference.

| Ipo | Target Mcap | Est Index Weight | Est Sp 500 Buying | Est Nasdaq 100 Buying |

|---|---|---|---|---|

| SpaceX | $1.75T | ~3% | N/A, denied June 4 (BI estimate of forgone bid: ~$14B) | ~$15–25B |

| Anthropic | $965B–$1T | ~1.5–2% | N/A, same profitability gate applies | ~$8–15B |

| OpenAI | $852B+ (last private) | ~1.5–2% | N/A, same profitability gate applies | ~$8–15B |

| Total potential | ~$3.6T combined | ~6–7% | N/A in 2026, earliest mid-2027 if profitable | ~$30–55B (NASDAQ-100 only) |

Every mega-IPO debate reaches for historical parallels. Three are worth knowing, quickly, because the table below holds most of the numbers.

Saudi Aramco (Dec 2019) is the closest size comparison: $1.7T valuation, $29.4B raise (with greenshoe), then ~+15% over the next six years while sector peers returned 55–65% and the S&P 500 returned 100%+. Being the biggest IPO doesn't make a stock the best buy. Size attracts attention; post-IPO performance is its own question.

Meta (May 2012) is the best lockup expiration precedent: IPO'd at $38, bottomed at $18 by September (–53%), didn't reclaim $38 until August 2013. But here's the part most coverage skips: Meta's biggest lockup-expiry (November 2012, ~800M shares) saw the stock rally +10% on the day. Same company, two lockups, opposite outcomes. Lockup direction is path-dependent.

Alibaba (Sep 2014) ran +220% by 2020, then lost ~65% peak-to-trough by 2022, almost entirely from China's regulatory crackdown, not the underlying business. Post-IPO returns can be dominated by exogenous factors that have nothing to do with fundamentals.

The pattern is variability. Aramco underperformed. Meta crashed then recovered. Alibaba ran then collapsed. Anyone telling you with confidence what SpaceX or Anthropic will do post-IPO is leaning on a pattern history doesn't actually offer.

Historical data shown; past performance does not indicate future results.

Key Takeaway: Mega-IPOs have produced everything from sustained underperformance (Aramco) to crashes followed by recovery (Meta) to rallies followed by external shocks (Alibaba). The pattern is variability, not direction.

Selected mega-IPO outcomes. Historical data shown; past performance does not indicate future results.

| Raise | Company | Ipo Date | Vs Sp 500 | Ipo Valuation | Six Year Return |

|---|---|---|---|---|---|

| $25.6B ($29.4B w/ greenshoe) | Saudi Aramco | Dec 2019 | Underperformed significantly | $1.7T | ~+15% |

| $16B | Meta | May 2012 | Outperformed long-term | $104B | +400%+ (recovered after -53% first year) |

| $21.8B | Alibaba | Sep 2014 | Outperformed then underperformed | $169B | +220% peak, -65% peak-to-trough by 2022 |

| Up to $75B | SpaceX (public Jun 2026) | Jun 2026 | Below $135 IPO price by mid-July 2026 | ~$1.75T | TBD |

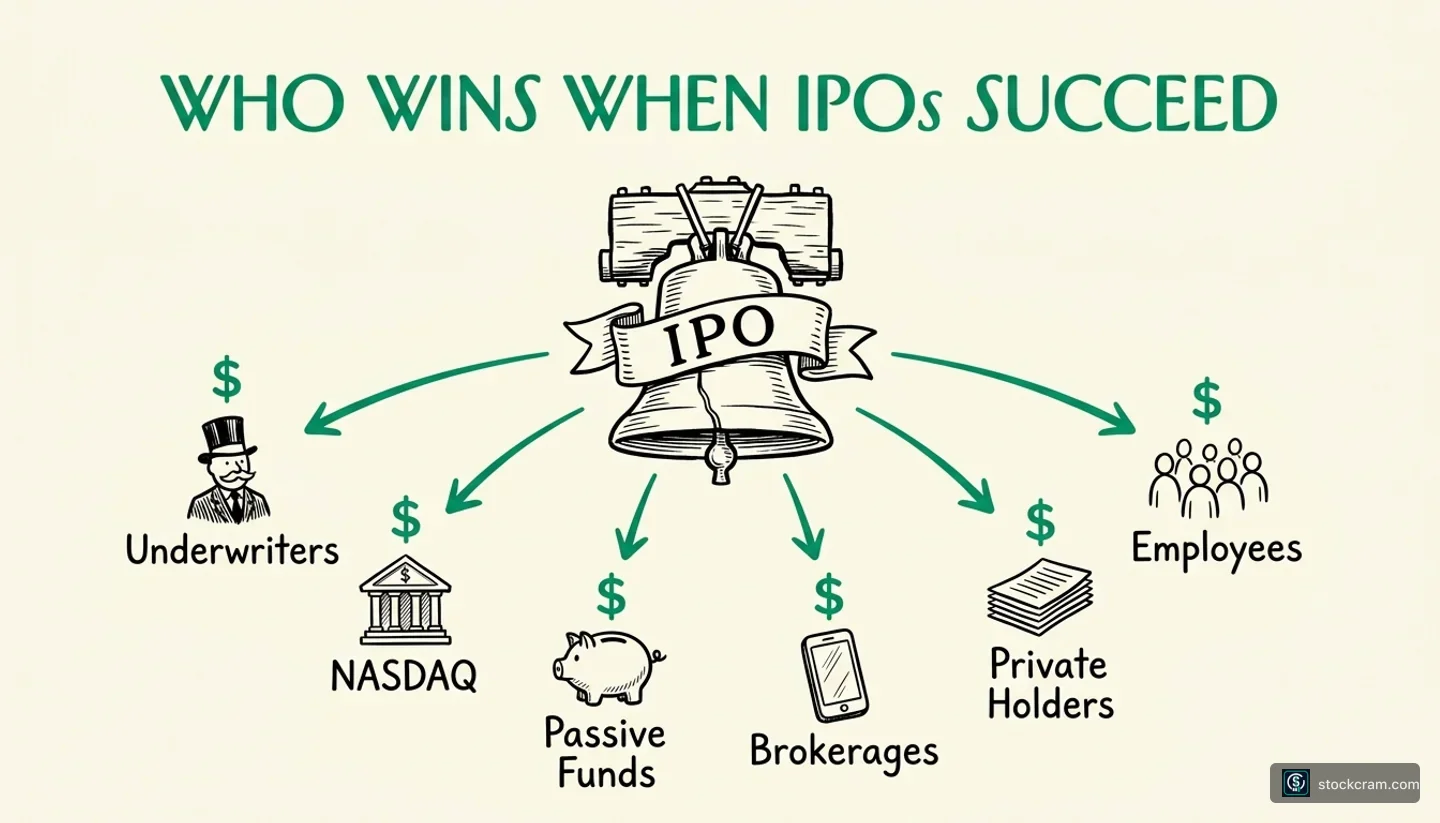

Independent of whether you think this wave is brilliant or reckless, it's worth knowing who wins regardless. IPOs aren't neutral events. They create immediate, structural winners across the financial system.

Six categories of winners, all collecting from the moment the IPO bell rings:

Each of these stakeholders profits whether the stock subsequently rises or falls. The list also doubles as a guide to whose forecasts you might want to discount accordingly.

The investment banks running the offerings. Goldman Sachs and Morgan Stanley are leading both Anthropic and SpaceX's syndicates (with JPMorgan in supporting roles). Underwriters typically take 4–7% of the IPO proceeds as their fee. On a $75B SpaceX raise, that's potentially $3–5 billion in fees split across the syndicate. Add Anthropic and OpenAI raises and the combined underwriting revenue could be the single largest IPO-fee year for Wall Street since 1999. Goldman and Morgan Stanley's 2026 earnings will reflect this whether the stocks subsequently rise or fall.

The exchanges. NASDAQ (where all three are reportedly listing) collects listing fees plus ongoing market-data and trading revenue from each name. Adding three top-40-by-market-cap members to its flagship NASDAQ-100 index is a structural prestige boost. NYSE loses, NASDAQ wins.

Passive index funds and their managers. This sounds counterintuitive: index funds are buyers, not sellers. But ETF issuers (BlackRock's iShares, Vanguard, State Street) collect management fees as AUM grows. The mechanical buying we covered earlier doesn't just move stock prices; it also flows into the fee base of the firms running the funds. The index machine has a vested interest in big new constituents.

Retail brokerages with IPO Access programs. Robinhood, Fidelity, and Charles Schwab all get user-acquisition wins from SpaceX's 30% retail allocation. (StockCram is not affiliated with any brokerage mentioned.) For Robinhood specifically, being the publicly-marketed retail channel for the largest IPO in history is a major brand event regardless of the stock's subsequent performance.

Existing private shareholders. Anthropic's earlier-stage investors (Google (14%), Amazon (8–16%), Nvidia (~3%)) see their private stakes become publicly-tradable. Same story for SpaceX's prior backers (Sequoia, Fidelity, Founders Fund) and OpenAI's (Microsoft, Tiger Global, others). These are paper-to-cash conversion events, with the timing controlled by lockup expirations.

Employees with equity. Anthropic has roughly 1,500 employees; OpenAI about 2,500; SpaceX north of 13,000. Most have meaningful equity stakes. An IPO doesn't immediately liquefy that equity, the 180-day lockup blocks immediate sales, but it converts illiquid private stock to a publicly-traded asset that can eventually be sold. The wealth-creation impact at the company level is substantial.

Knowing who wins regardless tells you something useful about who's incentivized to keep the wave moving, and whose forecasts you might want to discount accordingly.

Key Takeaway: Beyond the question of whether the IPOs deliver good returns for buyers, an entire ecosystem of banks, exchanges, fund managers, brokerages, and existing shareholders wins regardless. Knowing who's incentivized helps you read whose forecasts to take with extra salt.

Mainstream coverage often boils the bull case down to "AI is hot." The actual argument has named voices and specific claims.

Daniela Amodei, President of Anthropic, used a June 4, 2026 TechCrunch interview to address pre-IPO skepticism directly. Her core point was that the revenue is real and growing: Claude Code's $2.5 billion run-rate is enterprise demand from named customers, not vibes, and a continued trajectory would justify even aggressive valuations. Wedbush's Dan Ives, quoted in Fortune (June 2, 2026), called the Anthropic filing the "opening of the floodgates" for AI IPOs, a framing his desk has held publicly across the AI complex for over a year. On the institutional side, PIMCO's and BlackRock's June commentary (collated by TradingKey) is bullish on the AI infrastructure capex cycle; when two of the world's largest asset managers tell their clients to expect continued acceleration, the active-versus-passive money is broadly aligned with the wave rather than fighting it.

The strongest single point in the bull case is structural: this isn't 1999. Jay Ritter's IPO database at the University of Florida documents that only 28% of 1999 IPOs and 21% of 2000 IPOs had positive net income in their first year as public companies. The current wave looks structurally different: SpaceX has launch contracts and Starlink ARPU, Anthropic has a $47B run-rate with reportedly improving gross margins, and OpenAI has roughly $12B in ChatGPT consumer revenue. None of them are pets.com. That doesn't immunize them from drawdowns, but it changes the cash-flow math at the bottom of any selloff.

The index-mechanics piece reinforces part of the bull framing, though after the June 4 S&P decision, the bull side has to acknowledge it lost a meaningful amplifier. NASDAQ-100 Fast Entry and FTSE Russell's parallel changes still read as indexes catching up to a new reality where strategic companies stay private far longer than they used to; the old seasoning rules were systematically excluding the most important newcomers. Forced inclusion into NASDAQ-100 and FTSE indices, on the bull reading, isn't artificial pumping but a methodology fix that was overdue. The bulls' weaker hand is that S&P Dow Jones explicitly declined to adopt the same view, holding the S&P 500 to its existing profitability and seasoning rules.

Finally, SpaceX's 30% retail allocation is treated by bulls as a structural shift rather than a marketing decision. It's the first time U.S. retail investors will have direct IPO-price access to a trillion-dollar private-tech name, and that broadens who participates in the price discovery from Day 1.

Key Takeaway: Bulls aren't arguing the wave is small. They're arguing it reflects the maturation of a real AI economy with profitable, growing companies, not a speculative bubble.

The bear case has named voices and dated arguments too. The strongest version isn't "AI is fake." It's that timing, valuation, and historical pattern all point to late-cycle behavior.

Michael Burry has been the most direct, posting through May and early June 2026 on his Substack "Cassandra Unchained". His core line: "There is no guarantee, and not even a strong likelihood, that Anthropic is long-term worth anywhere near $1 trillion." He calls current AI demand a "false signal." Notable nuance, and a surprise, is that Burry does not think the IPOs themselves will mark the bull-market top. That's a position about valuation, not a crash call. Jeremy Grantham (GMO), interviewed in Fortune on May 19, 2026, used the phrase "blood in the streets," and has consistently put the probability that the AI bubble doesn't burst at "slim to none" across multiple appearances. Grantham's case is broader than the IPO wave specifically, but the wave is the most visible expression of what worries him.

The structural argument is harder to wave away. Mega-IPO clusters near market tops have a track record. Jay Ritter's IPO database shows only 28% of 1999 IPOs had positive net income in year one: the dot-com peak's signature wasn't unprofitability alone, it was unprofitable companies coming public in a cluster after a long bull run. Three trillion-dollar IPOs in four months at all-time highs in a single concentrated sector is the kind of thing that, in hindsight, often gets pointed at as the moment that mattered.

The valuation math compounds the timing concern. Anthropic at the $965B Series H number against a $47B run-rate is approximately 20.5× revenue, the upper end of comparable enterprise software (Nvidia ~25×, Snowflake ~12×) and a multiple that requires continued ~doubling of revenue year over year. If the pace breaks at any point in the next two or three years, multiple compression alone can produce 40–60% drawdowns even while the underlying business stays healthy. Layered on top is competitive risk: Anthropic competes with OpenAI (also filing), Google Gemini (free for many use cases), Meta Llama (open-source), Mistral, and xAI (now part of SpaceX). The "winner-take-most" assumption that supports premium multiples may not hold across the full stack, and coding, Claude Code's strength, is one of the most contested verticals.

The bear case also got a real-world data point on June 4: S&P Dow Jones publicly declined to relax S&P 500 eligibility rules for the wave, holding the line on profitability and seasoning requirements that SpaceX, Anthropic, and OpenAI all currently fail. That decision strips roughly $14 billion of forced S&P 500 buying out of SpaceX's first-year demand stack alone (per Bloomberg Intelligence), a quantifiable headwind that didn't exist a week ago.

The most disarming bear quote of the entire research pass came not from a bear but from the bull CEO. Dario Amodei, on Dwarkesh Patel's podcast in February 2026 (episode; Fortune coverage February 14): "If I'm just off by a year in that rate of growth, or if the growth rate is 5x instead of 10x, then you go bankrupt." When the CEO of an AI lab that's about to IPO at ~$1 trillion publicly flags bankruptcy as a possibility four months before listing, the bear case has been pre-conceded in part by the company itself.

Key Takeaway: Bears aren't arguing AI is fake. They're arguing the timing, the valuations, and the historical pattern all point to late-cycle behavior, and that even the bull CEOs are quietly flagging tail risk.

A possibility most IPO coverage skips: history suggests both sides may end up being right at the same time, just measuring different things on different time horizons.

The framing is unusual because it lets both sides keep their core argument intact:

Bulls and bears aren't disagreeing about the numbers, they're disagreeing about which numbers will matter three years from now. That distinction is what makes "both sides right" historically common.

The internet was a real, world-changing technology and the dot-com bubble was real. Both descriptions of 1995–2002 hold up. The technology was transformative; the stock-market expression of it was a bubble that destroyed enormous amounts of capital. Cisco was the dominant, profitable infrastructure company at the heart of the internet revolution, and Cisco's stock still fell about 85% from its 2000 peak. Those facts coexist without contradicting each other.

The mega-IPO comparable suggests the same dual outcome can apply at the company level. Saudi Aramco is a real company that pumps real oil and generates real cash; it was the biggest IPO in history; and it underperformed the S&P 500 by roughly 4× over the six years that followed. The company is structurally important. The stock was a poor buy at IPO. Neither claim cancels the other.

If that's how the AI IPO wave resolves, the most likely outcome is that the companies remain strategically important and deliver disappointing 5-year stock returns relative to the S&P 500. SpaceX could be a Tesla-style story where the company is foundational but the stock has multi-year drawdowns along the way. Anthropic could be a Cisco analogue: profitable, dominant, still down 70%+ from peak at some point in the next decade. OpenAI's governance complications could compound either outcome.

In that scenario, Burry could be right that current valuations leave no margin for execution risk, while Daniela Amodei is simultaneously right that the underlying business compounds for decades. The bears would be right about prices in the next few years; the bulls would be right about long-term importance. The two views aren't actually in conflict. They're measuring different things on different clocks.

That's not a comforting framing. It's just the historically most common one when a real innovation meets an enthusiastic market.

Key Takeaway: A real revolution can produce real winners and still produce dramatic losses for investors who paid too much. "Both sides right" is historically more common than "one side right."

Both sides have concrete signals they're watching over the next 12 months. The list below is the framework we'd recommend bookmarking: these are the events that will move the debate, not the daily price action.

Key Takeaway: Each side has concrete events to watch. Which list moves first will likely tell us whether this wave was a top or a launch.

Same article in one screenshot. Bookmark this and check back each quarter.

| Signal | Bears Watch | Bulls Watch |

|---|---|---|

| First-day pricing (SpaceX) | Below $1.75T target, heavy first-week sell-off | At-or-above target, strong institutional book |

| AI revenue growth | Anthropic / OpenAI run-rate deceleration | Continued >50% YoY across all three |

| Lockup expiration | Heavy insider selling pressure 6 months post-IPO | Orderly transitions; Meta-style biggest-lockup-rally outcome |

| Enterprise AI traction | S&P 500 cos still report no productivity impact from AI | Non-tech S&P 500 cos attribute margin gains to AI |

| Tesla-SpaceX merger | Merger collapses → SpaceX valuation re-rates lower | Merger confirmed → combined-entity premium expands |

The wave isn't three independent IPOs. Each one signals to the next. SpaceX's first day was the loudest single signal in the sequence, and the systemic consequences of strong vs. weak pricing are worth thinking through. As it turned out, SpaceX priced at $135, popped, then slid below its IPO price by mid-July, and the sequence has broadly followed the weaker-case path described below: OpenAI pushed its listing toward 2027 while Anthropic kept to its October track. The framework is retained here for how to read a debut's knock-on effects.

If SpaceX prices strong (open materially above $135, sustained institutional bid, NASDAQ-100 inclusion absorbs cleanly within the first 15 trading days) the cascade likely goes something like this. Anthropic's underwriters get pricing power, and the amended S-1 valuation (currently media-inferred at $965B from the May Series H) likely lands at or above that figure rather than below it. OpenAI's confidential filing moves toward a firmer listing timeline rather than slipping further out. A second cohort of late-stage AI companies (xAI's former peers, infrastructure plays, Anthropic's competitive layer) starts evaluating its own IPO timing. The wave widens; the bull thesis gains a tape-tested data point.

If SpaceX prices weak (open at or below $135, heavy down-halts in the first session, NASDAQ-100 inclusion meets a soft mechanical bid) the cascade goes the other direction. Anthropic's underwriters lose pricing power and the amended S-1 may signal a more conservative target. OpenAI may delay disclosure and let SpaceX's tape mature before committing to a date. Late-stage AI companies pause IPO planning. Broader AI-sentiment indicators (cloud-AI revenue growth deceleration, hyperscaler capex revisions) start being scrutinized more aggressively, and the bear thesis gets the validation it's been waiting for.

Neither scenario is automatic. Mega-IPOs have surprised in both directions historically: Meta opened modestly above its IPO price and still cratered weeks later; Aramco opened flat and then materially underperformed for years. The point isn't to predict which scenario unfolds; it's to know in advance which signals would matter and which would just be noise.

Key Takeaway: The wave isn't three independent events; it's a cascade. SpaceX's Day-1 sends the loudest signal forward to Anthropic and OpenAI, and the cascade direction is what readers should watch.

Mega-IPO waves are rare. Putting the 2026 AI wave alongside the three prior waves that genuinely reshaped capital markets is the cleanest way to read what's unusual about it and what isn't.

Key Takeaway: Every prior wave had a real underlying thesis and a stock-market expression that overshot it. The honest 2026 read is that the underlying thesis is real and the question is overshoot, not validity.

Each wave was defined by a single dominant theme that reshaped the listing market for years. Outcomes shown are post-wave returns over the following ~5 years.

| Wave | Core Thesis | Anchor Companies | Peak Year Outcome |

|---|---|---|---|

| 1999-2000 dot-com | Internet would reshape every business | Amazon, Pets.com, Webvan, Cisco peak | NASDAQ -78% from peak by Oct 2002 |

| 2012 social media | Networks would monetize attention at scale | Facebook (Meta), LinkedIn, Twitter | Long-term thesis right; near-term mixed (Meta -53% first year) |

| 2020-2021 SPAC | Faster, retail-friendly path to public markets | Lucid, Virgin Galactic, DraftKings, Trump Media | Index of de-SPACs -75%+ by 2023 |

| 2026 AI IPO wave | AI infrastructure + foundation-model layer goes public | SpaceX, Anthropic, OpenAI | TBD |

Strip away the disagreement and three points keep showing up in both camps' research: the wave's scale is unprecedented, the NASDAQ-100 Fast Entry mechanic will apply real mechanical buying (now without the S&P 500 amplifier after S&P's June 4 decision), and Anthropic's revenue trajectory is real (Burry disputes the valuation, not the numbers).

Which narrows the actual question. The reality of AI is settled across both camps. The scale of the wave is settled across both camps. The unresolved question is whether current target valuations already reflect the risks both camps see. Bears say no: valuations leave no margin for execution issues, and the loss of S&P fast entry removes a tailwind that was already priced in. Bulls say yes: valuations reflect achievable growth from companies actually delivering, and the NASDAQ-100 mechanic is intact. That gap is what the next twelve months of revenue numbers and price action will close.

Key Takeaway: Bulls and bears are arguing about the consequences of the same facts, not about the facts.

Most IPO articles end with a verdict. We won't, and the reason is practical.

Mega-IPO outcomes have historically gone every direction. Aramco underperformed for years. Meta crashed then recovered. Alibaba ran then collapsed for reasons unrelated to its business. Anyone telling you with confidence what SpaceX, Anthropic, or OpenAI will do at one-year, three-year, or five-year horizons is leaning on a pattern history doesn't actually offer.

A more useful question than "is the wave a bubble?" is what would have to be true for each case to play out? For the bull case to hold, AI revenue growth needs to continue roughly at current pace, the new index mechanics need to translate into real long-term institutional support, and the broader AI economy needs to deliver measurable productivity gains at non-tech S&P 500 companies. For the bear case, revenue trajectories need to break, lockup expirations need to test holding patterns, and the index-inclusion bid needs to fade once initial buying is done. Watching those specific things, the watchlist a few sections back, is more useful than watching the daily SpaceX close.

The most disarming single line from the entire research pass came from the bull side. Dario Amodei, on the Dwarkesh Patel podcast (February 2026): "If I'm just off by a year in that rate of growth, or if the growth rate is 5x instead of 10x, then you go bankrupt." When the CEO of an AI lab that's filed for a roughly $1 trillion IPO publicly flags bankruptcy as a tail risk four months before listing, the framing of "settled bull thesis" gets harder to maintain.

For beginners specifically: read the S-1s when they become public (especially OpenAI's, which will be the most strategically loaded). Watch the validators in the watchlist above. Decide for yourself whether you want exposure, and at what position size you'd be comfortable holding through a meaningful drawdown.

If you want to go deeper on how stocks are valued in the first place, the Foundations course is the starting point. If you want to apply a multiple to these companies once they're trading, the P/E ratio calculator is the quick tool for that.

Key Takeaway: Smart investors disagree because the AI IPO wave's outcome can't be called in advance. Holding that uncertainty without panicking is the actual skill.

Five common misreads. None of these are dumb questions: they're the questions the headlines invite.

"If I buy on day one, I'm getting in at the IPO price." No. The IPO price is allocated to institutional clients of the underwriters. Retail investors typically buy at the market price after the first trade, which can be above the IPO price (a "pop") or below it (a "break"). The IPO price is what insiders get; the open price is what you get.

"A bigger IPO is a better company." Saudi Aramco was the biggest IPO in modern history in 2019 and underperformed the S&P 500 by roughly 4× over the six years since. Size attracts attention; quality is a separate question.

"Lockup expirations always crush the stock." Sometimes. Meta hit its post-IPO low at its first lockup expiration in 2012. But Meta's biggest lockup (November 2012, ~800M shares) actually rallied +10% on the day. Path-dependent.

"Confidential filings hide bad news." No, confidential filings are a JOBS Act provision. Roughly 80% of recent IPOs filed confidentially first. It lets companies refine their S-1 drafts with the SEC privately before the offering becomes public. Anthropic and OpenAI filing confidentially is procedurally normal, not suspicious.

"Index inclusion = automatic gains." Mostly tailwind, but not magic. Tesla rallied ~70% after its S&P 500 inclusion in December 2020 with an estimated $51B of mechanical buying behind it (S&P Dow Jones indexology notes; bank-desk estimates at the time). But Snowflake and DoorDash both underperformed in the year following their NASDAQ-100 additions. The mechanical bid is real; everything else is up to the underlying fundamentals.

For more current-market reads on the broader picture, the rest of the Market Explainers series covers the AI bubble debate and other confusing market moments with the same both-sides approach.

Key Takeaway: Most beginner confusion about IPOs comes from treating the IPO as the end of the story. It's the start.

Quick answers to the questions readers ask most about the AI IPO wave.

Selected primary sources for the figures and quotes used in this article. The IPO analysis is easier to follow when you've seen the actual filings and the original interviews. Links go to publication homepages and primary documents where we've verified them; specific article URLs are described inline so you can search them directly without having to trust a redirect.

Company filings / market data

Bear research

Bull research

IPO research / academic

Historical mega-IPO comparisons

Index mechanics

SpaceX IPO mechanics

Last reviewed: July 26, 2026.

The wave is unprecedented in scale.

Roughly $3.6 trillion in combined target valuation across three companies in a four-month window. Neither bulls nor bears dispute the size.

The killer mechanic is forced index buying, but smaller than first reported.

NASDAQ-100 Fast Entry (effective May 1, 2026) auto-includes top-40 names after just 15 trading days, plus FTSE Russell's parallel fast-entry rules. On June 4, 2026 S&P Dow Jones declined to relax S&P 500 entry, removing what would have been the largest amplifier (Bloomberg Intelligence estimates ~$14B of forgone forced buying for SpaceX alone). The NASDAQ-100 + FTSE mechanic is still real and mandatory, in the tens of billions across the wave.

Bulls and bears cite the same facts.

Anthropic's $47B run-rate, SpaceX's $1.75T target, the new index rules, all agreed. The disagreement is about what those facts will mean three years from now.

Each side has a concrete watchlist.

Bears watch SpaceX day-one pricing, AI revenue deceleration, lockup expirations. Bulls watch institutional allocation, non-tech AI productivity attribution, on-schedule index inclusion. Which list moves first will settle the debate.

Both sides may end up being right.

History suggests technology revolutions often coexist with stock-price corrections. Aramco was a real company that underperformed. Cisco was a real company that fell 85%. AI may follow the same dual pattern: companies remain important, stock returns disappoint.

Even the bull CEO flagged the bear case.

Anthropic's Dario Amodei publicly said "If I'm just off by a year in that rate of growth… then you go bankrupt." When the bull-side CEO names bankruptcy as a tail risk four months pre-IPO, you can take both sides seriously.

Robinhood agentic trading lets an AI agent place trades in a dedicated, funded account. A calm, plain-English walkthrough of how it works and the risks.

A war headline turned your portfolio red and your finger is over the sell button. Here is a calm, educational look at panic selling and how to tell a reaction from a plan.

Is the housing market crashing in 2026? The truer answer: it's frozen, not crashing. The lock-in effect, both sides, in plain English.

Approximate share of total S&P 500 market capitalization as of May 2026. Source: MacroMicro. Adding SpaceX / Anthropic / OpenAI compounds the concentration.

Annualized monthly revenue (run-rate), Jan 2024 to May 2026. Sources: Simon Willison (May 29, 2026); CNBC (May 28, 2026).

SpaceX has now traded, so this is history rather than a prediction. It priced at $135 for a ~$75B raise (the largest IPO in history), with a reported 30% retail allocation through Robinhood, Fidelity, and Schwab (StockCram is not affiliated with any brokerage mentioned). It began trading June 12 on NASDAQ as SPCX, closed Day 1 at $160.95 (+19%) and reached $225.64 on June 16, then fell back below its $135 IPO price by mid-July, trading around $113 on July 25 (an all-time low of $110.85 on July 23). The debut has been rocky. Historical data shown; past performance does not indicate future results.

Nobody can answer that without understanding your goals, time horizon, and risk tolerance, and you should be skeptical of anyone who answers it confidently. What investors typically do when uncertain about an IPO: review position sizing (would this be 1% or 10% of your portfolio?), check whether the valuation multiple is defensible at any reasonable assumed growth rate, and consider whether you would be comfortable holding through a 50% drawdown without panic-selling. Anthropic is currently trading at roughly 20.5× revenue based on the $965B Series H number, at the upper end of comparable enterprise software. Tools that help: our P/E ratio calculator, the Foundations course.

OpenAI filed confidentially on June 8, 2026, but has since delayed. Recent reporting (Bloomberg, June 26, 2026) now points to a 2027 listing rather than a 2026 debut, citing market volatility, SpaceX's rocky public debut, and CEO Sam Altman's insistence on a roughly $1 trillion listing floor. Altman publicly says he's "not focused on timing." The amended S-1 (which becomes public approximately 21 days before the roadshow) will be the moment the numbers turn from inference into disclosure. Until then, everything about OpenAI's IPO valuation, governance disclosure, and Microsoft equity arrangement is media inference, not prospectus statements.

SpaceX trading publicly creates a market price for what is reportedly Elon Musk's largest private holding. If the Tesla-SpaceX merger reports materialize (Dan Ives at 80% odds; Fortune June 4, 2026 spotted a hint in SpaceX's amended S-1), the combined entity would be approximately $3.4 trillion in market cap. Per Electrek's analysis, the merger would also reportedly trigger Musk's $1 trillion Tesla compensation package automatically. Treat as material rumor, not confirmation. There has been no official Musk statement on the record.

For most retail investors, you usually don't. IPO pricing is allocated to institutional clients of the underwriters (the investment banks running the offering). Retail allocation programs exist (Robinhood IPO Access, Fidelity's program, and Schwab) but allocation is uncertain and typically small. The practical retail path to most IPOs is buying at the open price on day one, which can be above the IPO price (if there's a "pop") or below it. SpaceX's unusually large 30% retail allocation is an exception to the typical pattern. See the dedicated section above for more on the retail paths into SpaceX specifically.

Effective May 1, 2026, newly listed companies that rank in the top 40 by market capitalization can enter the NASDAQ-100 after just 15 trading days of seasoning, no prior liquidity requirements. Previously, names typically had to season for around six months. The change matters because passive index funds tracking the NASDAQ-100 will *mechanically buy* the new index members within weeks of IPO, regardless of fundamentals. Important update: S&P Dow Jones announced on June 4, 2026 that it would *not* relax the S&P 500's parallel requirements, meaning SpaceX, Anthropic, and OpenAI are blocked from S&P 500 fast entry until they meet existing profitability and seasoning rules (earliest mid-2027). FTSE Russell has adopted fast-entry rules, so SpaceX is also eligible there. The total NASDAQ-100 + FTSE Russell mechanical buying across the wave is on the order of tens of billions, meaningful but smaller than the trillions-of-dollars figure that was circulating when S&P fast entry was thought to be in play.

Realistically, in hindsight. Bears (Burry, Grantham) argue mega-IPOs concentrated in one sector at all-time highs are textbook late-cycle. Bulls (Daniela Amodei, Dan Ives, PIMCO) argue these are profitable companies with real revenue (unlike 1999 dot-com IPOs), and the index-inclusion rule changes reflect index methodologies catching up to a private-market-heavy era. Both sides have real data. The question history doesn't answer in advance is which set of facts will dominate the next 3-5 years of returns.

SpaceX has the most diversified revenue base (Starlink subscriptions, launch contracts, xAI integration). Anthropic has the highest revenue growth trajectory (~500× run-rate growth in 18 months). OpenAI has the highest consumer revenue (ChatGPT) but the lowest current profitability and the most complex governance structure (Microsoft equity, non-profit-controls-for-profit). They're different bets in the same orbit, not interchangeable. The article above does a section-by-section breakdown.