Three Ways to Test the Same Strategy

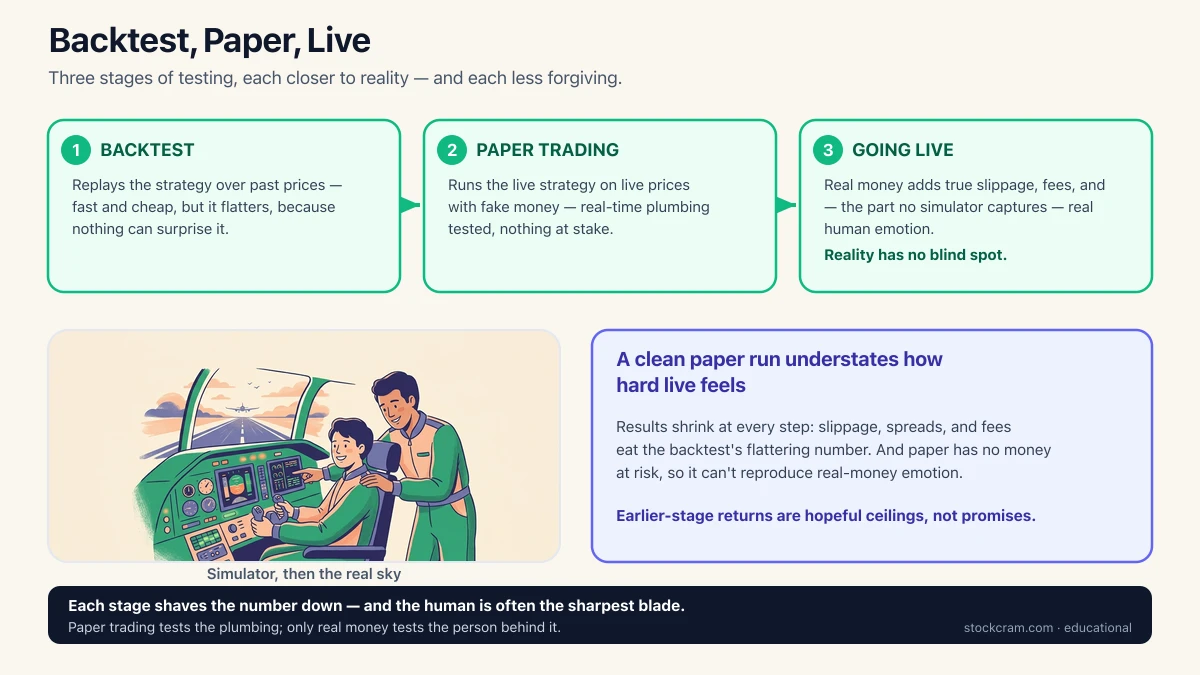

Before a strategy ever touches real money, it usually passes through three stages of testing — each one closer to reality than the last. The first is backtesting: replaying the strategy over past price data to see how it would have done. It's fast and cheap, but it flatters, because the past is already known and nothing about it can surprise you.

The second stage is paper trading — also called forward testing. Here the same strategy runs on real live prices, in real time, but with fake money. Nothing is at stake, and the clock ticks in real time — close to how it would with real cash, even though the fills themselves are simulated and may not match what real money would get. The third stage is live: real money, real slippage, and — the part no simulator captures — real emotions. Think of it as three ways to prepare a pilot: a backtest is studying footage of old flights, paper trading is a flight simulator, and going live is actually leaving the ground.

The One-Sentence Version

Backtesting asks "would this have worked?", paper trading asks "does the machinery actually run in real time?", and live asks "does it survive real money, real costs, and a real human watching?" — three different questions, in rising order of difficulty.

Why Paper Trading Isn't Optional

A backtest can show whether the idea behaved plausibly under historical assumptions and expose obvious weaknesses. It can't prove the plumbing works, because a backtest never places a single live order — it just does arithmetic over a spreadsheet of history. Paper trading is where the plumbing gets tested: Does the code place orders in the correct format? Does it notice and recover when the connection to the broker drops for thirty seconds? Does it log every fill so you can see what really happened? These are real-time questions, and only a real-time run can answer them.

A backtest can't catch a live bug

If your order-placing code has a bug — say it accidentally sends the same order twice — a backtest will never reveal it, because a backtest doesn't place orders. Paper trading runs that exact code against the live market, so the double-order shows up harmlessly in the logs instead of expensively in your account. That's the whole point of the stage.

The Three Stages Side by Side

Each stage uses different inputs, risks a different amount, and is good at catching a different class of problem. Lined up next to each other, the ladder — and each rung's blind spot — becomes clear:

| Dimension | Backtesting | Paper trading | Live |

|---|---|---|---|

| Data used | Past, recorded prices | Live prices, in real time | Live prices, in real time |

| Money at risk | None | None (fake money) | Real money |

| Best at catching | Broken logic and weak ideas | Code bugs, disconnects, timing issues | True slippage, fees, and emotion |

| Main blind spot | Everything about real-time execution | Realistic fills, queue position, market impact, fees, and the emotional cost of real money | Statistical confidence and rare market conditions it hasn't faced yet |

Each stage narrows the previous stage's blind spots, but none removes them all — paper still can't reproduce real fills or real emotion, and even live can't rule out market conditions it hasn't met.

The bottom row is where it clicks: no single stage is enough. A backtest is blind to real execution; paper trading narrows that gap but still misses realistic fills, queue position, market impact, fees, and emotion; live is where real execution finally happens — which is exactly why it's the least forgiving, though even live can't rule out rare market conditions it simply hasn't met yet. Skipping straight from a backtest to live means shipping untested plumbing and an untested nervous system at the same time.

The Backtest-to-Live Gap

Results tend to shrink at every step down the ladder, and the reasons stack up. Real slippage means you rarely get filled at the exact price you saw — the market moves in the moment your order travels. The bid-ask spread quietly taxes every round trip. Fills aren't guaranteed at all when there aren't enough buyers or sellers, market impact nudges the price against you as your own order lands, and fees add up trade after trade. A backtest can estimate these, but it usually estimates them too kindly.

Then there's the biggest variable of all, and it only appears in the last stage: the human. Paper trading feels calm because nothing is lost when a trade goes wrong. Move the same strategy to real money and a losing streak that a simulator shrugs off can become the moment someone overrides the system, closes a position early, or switches it off at the worst time. Because paper trading removes the emotional variable entirely, even a flawless paper run understates how hard live trading feels — the simulator can't make your stomach drop.

A Worked Example: How the Number Shrinks

Take a stylized, made-up strategy and watch its headline return erode as it moves down the ladder — all numbers below are illustrative only and, as always, past results don't predict future ones.

- Backtest: +12%. Replayed over last year's recorded prices, the strategy shows a tidy +12%. Fills are assumed to happen at the exact prices in the data, and costs are estimated generously.

- Paper trading: about +8%. Run live for a few weeks on real-time prices, the same rules earn less. Real timing bites — some orders that filled instantly in the backtest now miss, and a couple of fills land at slightly worse prices.

- Live: less again. With real money, true slippage and the bid-ask spread shave the number further, fees accumulate, and during one sharp drop a nervous human manually overrides the system and closes a trade early — locking in a loss the rules would have recovered.

The exact figures are invented, but the shape is the lesson: each stage tends to shave the number down, and the human is often the sharpest blade. A strategy that only barely works in a backtest can easily cross into losing money by the time it reaches the real world.

Going Live, Carefully

None of this is a set of instructions — it's a description of how careful practitioners tend to approach the transition, framed as concepts, not steps to copy. The pattern is roughly the same wherever you look. People who move carefully tend to start tiny, putting so little money at stake that a bug or a bad streak is a cheap lesson rather than a painful one. They keep every guardrail from the risk lesson switched on — position limits, the drawdown cap, the kill switch — precisely because live is when those brakes matter most.

And they compare reality against the model: lining up live fills next to what the backtest and paper run expected, to see whether the strategy is behaving as designed or quietly falling apart. If live results diverge sharply from paper, that's information — a sign the model missed something real. The theme running through all of it is humility: treat the numbers from earlier stages as hopeful upper bounds, not promises, and let reality have the final word.

One way to hold all of this in your head is to remember what each stage mainly tests and what it still misses — because no stage answers every question, and each one exists to close a gap the last couldn't:

| Stage | What it mainly tests | What it still misses |

|---|---|---|

| Backtest | Historical logic | Future regimes and real execution |

| Paper | Workflow, timing, and system behavior | Realistic fills, queue position, impact, and emotions |

| Small live | Actual execution and operational behavior | Statistical confidence and rare regimes |

| Scaled live | Capacity and larger-order effects | Future market changes |

Each stage mainly tests one thing while staying blind to another — which is why careful practitioners tend to move through them in order rather than skipping ahead.

Educational use only

Educational content only. StockCram isn't a broker or adviser, and we have no affiliation with any institution or tool we mention. Nothing here is a recommendation to trade in any particular way.